Budgeting During Inflation in Canada

Introduction

There are many reasons why inflation occurs. Food and fuel prices are often considered the biggest culprits, but the average consumer’s spending habits can play a big role as well. Inflation is inevitable and there’s no way to stop it, but that doesn’t mean you have to spend more money than you need to just because prices go up over time. It’s important to be prepared for inflation as best you can so that it doesn’t hurt your budget too much or even worse, put you into debt!

Being prepared

- Being prepared: The most important thing you can do is to draw up a budget and plan for the future. As inflation creeps in, you want to make sure that your income keeps pace with it and doesn’t lag behind. This means planning ahead so that you can save more money when things are good, but also being flexible enough so that when things go awry (as they inevitably will), there’s still some cash flow left over each month.

- Saving enough money: If your income is steady, then saving is easy—just set aside what’s left at the end of each month for savings or investments and keep doing it until it becomes habit! However, if your income varies from month-to-month or week-to-week (sometimes even day-to-day), then saving may be more difficult because sometimes there won’t be any money left over after covering expenses like rent/mortgage payments or groceries; this is where having an emergency fund comes in handy!

Look at your mortgage

If you have a fixed-rate mortgage, consider refinancing if rates drop. The longer the term of your mortgage, the better it is to refinance at lower rates. If you’re already in a variable rate, look into getting a fixed or capped rate that matches your current mortgage if rates drop.

Get ahead of things

Inflation is a tricky beast. It can sneak up on you without you even realizing it, and before you know it your budget is in shambles. It’s important to stay on top of inflation so that your financial situation doesn’t fall apart!

- Look at your budget: If you’ve done a good job of tracking where your money goes each month, then this may be a breeze for you. If not, we recommend using an app like Mint or Quicken to track expenses for at least two months to get a better idea of how much money comes in versus how much goes out. Once that’s complete, create categories where appropriate and try to come up with some creative solutions if there are any red flags (for example: “Eating Out” might be too high).

- Look at other areas of spending: Are there any areas where we could cut back? Where are our priorities? Is there anything else we could eliminate completely? This step will likely take some time—and possibly some tears—but setting aside personal luxuries means that when inflation hits hard again next year (or sooner), we’ll still have enough saved up for those rainy days.*

Save on food

If you are looking to save on food, there are some easy ways that you can do this. The first option is to buy in bulk. This will allow you to get a lot of the same product at once and then store it for later use. It may also be more cost effective than buying smaller quantities throughout the month or week.

Another good way to save money is by looking for sales and coupons from various stores that sell similar products, particularly grocery stores and supermarkets. You can also look for cheaper alternatives like lower quality items or cheaper brands than what you normally buy as well as cheaper stores and meal options like eating out less often or cooking your meals at home instead of ordering out on nights when possible (which will save even more money).

Buy cheaper brands

There are many ways of lowering your grocery bill without sacrificing quality. Some options are as simple as buying generic brands, while others might require some planning and preparation. Here’s a list of tips to keep in mind when shopping for groceries:

- Buy store brands instead of name-brand products

- Buy in bulk when possible (e.g., at Costco)

- Buy in season or on sale

- Buy on Amazon (if you have a Prime membership)

Use coupons

Coupons are one of the easiest ways to save money on your groceries, and they’re also a great way to save money on other items you purchase. You can find coupons in newspapers, magazines, online and in stores. Coupons typically allow you to buy an item at a lower cost than normal price; however some coupons may even include free products!

The following are some examples of how you can use coupons:

- Use them as currency for trading within your community (e.g., swapping clothes with friends).

- Give them away as gifts for birthdays or holidays.* Don’t throw away expired ones! They still have value!

Cut back on eating out

Eating out is a luxury, so you should cut back on it when times are tough. The best way to do this is to eat at home more often and only eat out less often. If you do decide to go out, try eating at cheaper restaurants or even fast food chains like McDonald’s or Burger King. You’ll save yourself some money and get some good value for your buck.

Buy generic brands

- Generic brands are usually cheaper

- Generic brands are usually the same quality as brand names

- Generic brands are usually available at the same stores as brand names

Take stock of your bills

To start, list all of the monthly bills you pay. These include things like rent or mortgage payments, car insurance and gas costs, grocery bills and utility bills (water/electricity). Next, figure out how much money you spend on each bill per month, per year and even per week/day/hour if possible.

Now that you have a clear picture of how much money is going out every month, we can begin to identify potential areas where we can cut back on spending.

Reconsider utilities

One of the first things you should do as a budgeter is to look at your utility bills. Look for anything that can be done to lower your cost, whether it’s changing providers, using less electricity or water, or switching from heating oil to natural gas. If you find yourself driving long distances every day for work and need to cut back on gas usage, consider taking public transportation instead of driving yourself (or maybe even getting rid of one car altogether).

Inflation is inevitable, but that doesn’t mean you can’t plan ahead.

Inflation is a natural process that occurs when the supply of money grows faster than the demand for it. When this happens, prices rise and the purchasing power of your money decreases.

Inflation does not happen overnight; it takes time for inflation to increase from 0% to 2%. And it’s important to remember that inflation is not just something that affects you and me as consumers in our day-to-day lives, but also affects businesses who need to adjust their prices accordingly in order to stay competitive in the market place.

However—just because we know what causes inflation doesn’t mean we have control over how much it will occur or when! Inflation can be very unpredictable so we all have a role here: stay informed about current economic news so you can plan ahead accordingly!

Conclusion

With inflation being a fact of life, it’s important that you take steps to plan for it. By being prepared and looking at ways in which you can cut back on spending when prices go up, you can avoid getting caught off guard when your grocery bill suddenly goes up or electricity rates increase without warning.

Get Your Credit Report in Canada for Free

Introduction

You may not realize it, but your credit report is probably the most important financial document you own. It dictates how much you pay for things like car loans and mortgages, whether or not you can get approved for new credit cards and loans, and even if you’re eligible for certain jobs. The more time goes by without checking your credit report, the higher your risk of making mistakes that could cost you big bucks down the road. In this guide we’ll show you where to go to access your free credit score and report in Canada — as well as how to read it so that no matter what grade score you land on (or don’t), there’s always room for improvement!

For those of you who don’t know, a credit report is a document that provides information on your credit history and shows whether or not you have any outstanding debts. Your credit score is a number generated by looking at your history, which lenders use to determine whether or not they should offer you loans.

Credit Score vs. Credit Report

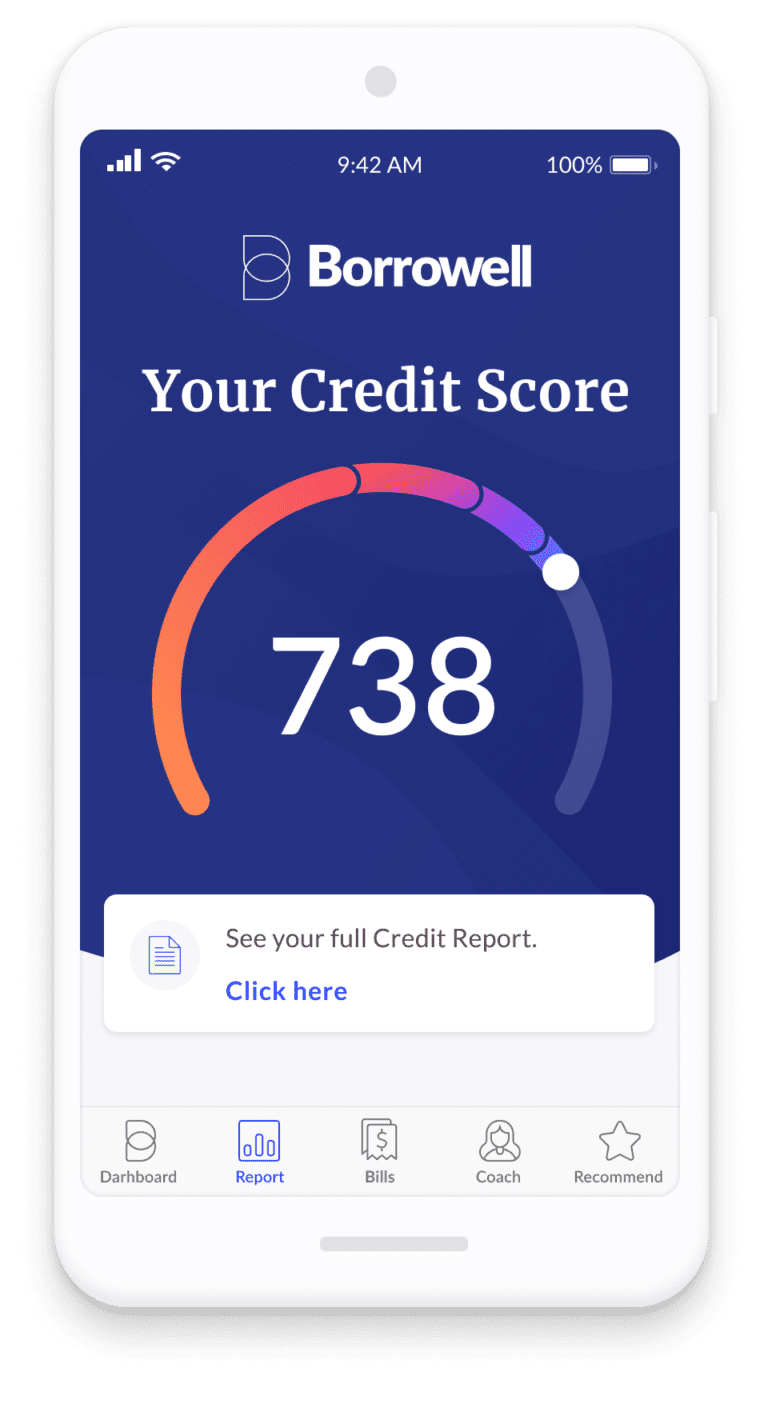

Did you know that your credit score is not the same as your credit report? Credit score is a three-digit number between 300 and 850. It’s based on the information in your credit report, but it’s used by lenders to determine whether or not to lend you money or give you a loan. Your credit report is a history of all of your credit activity, including things like paying bills on time and using too much of your available credit (what’s called “maxing out”). A snapshot of this information can be found on any website that provides free access to detailed reports; however, most sites will only provide partial information. The best way to get an accurate picture of where you stand financially—and take steps toward better financial health—is by requesting a full copy from Borrowell.

Why check your credit report?

Checking your credit report is important for a number of reasons:

- You can see if there are any errors.

- You can see if you have been denied credit.

- You can see if you have been overcharged for credit.

- You may be able to spot unauthorized accounts or collections on your report that need to be removed, which will improve your score and help you get approved for more things in the future (like an apartment or car loan).

Where to access your free credit score and report in Canada

There are a few ways to do this, but we’ll review the most common option today:

Use Borrowell This service let users sign up for an account online and then provide immediate access to their scores and reports at no cost.

How to read your credit report in Canada

Credit bureaus are the companies that keep track of your credit history. They evaluate how you’ve used your credit and assign a score to help lenders better assess whether they should give you a loan or not.

Here’s how to read your credit report in Canada:

- Understand the difference between a credit score and a credit file

A “credit score” is an artificial number assigned by one or more companies that keeps track of how well you manage money. A “credit file” is what the company uses to calculate this number; it includes all details about past loans, any unpaid bills, and any court judgments against you (even if they’re settled). If there are errors on either one, it can affect whether you qualify for financial products like loans or mortgages at fair interest rates.

Conclusion

In the end, it’s important to remember that your credit report is a snapshot of your credit history. It’s used by lenders when deciding whether or not you qualify for loans and credit cards, so it’s worth checking at least once a year. You can do so through Borrowell—a company that offers free access to your credit report.

If you want to take things a step further and ensure your score stays high all year round, consider using one of these tips:

- Pay off debts on time every month. Don’t miss any payments!

- Try to get some positive items on your accounts (like making all payments on time). If there aren’t any positive items already on the account, see if there are any negative ones that could be removed by calling in or sending an email directly from their website (more details below). These types of reports give lenders an idea about how responsible someone has been with their finances overall—and since they’re used as part of calculating scores for everything from loans and mortgages down through small business financing options like SBA loans (which help entrepreneurs start up new businesses), having good qualifications here can make all kinds of difference when applying for credit products down the road!

Everyone should check their credit report at least once a year, you can do it for free through Borrowell

With Borrowell, you can check your credit score and report for free. You’ll get a better understanding of where things stand so you can make informed decisions now, and in the future.

This is a great way to start planning for your next big purchase or financial goal!

How? We’re glad you asked:

- Sign up with Borrowell . This takes about 5 minutes total – don’t worry if you don’t have an existing account with them.

- Once this step is complete, log into your dashboard . On this page you’ll see information about how lenders view each aspect of your credit score and how it could affect your ability to borrow money (or not). If there are any changes since last year’s scorecard was generated they’ll be highlighted here along with explanations as needed.”

Conclusion

There are many ways to improve your credit report and score, but the most important thing is that you do it. It’s always good to have an idea of where you stand so that you can take steps towards improving your situation. If you’re looking for more information about how to manage your money, check out our blog! https://www.ccdr.ca

How to deal with Bill Collectors in Canada

Introduction

If you are receiving calls from a collection agency, it’s likely because you have an unpaid debt. Collection agencies must follow strict rules when collecting unpaid bills from individuals in Canada. The key to dealing with collection agencies is to know your rights and keep everything in writing.

DO ANSWER THE PHONE.

- Never ignore a bill collector’s call. It may seem like the easiest way to deal with an annoying situation, but you can’t avoid bill collectors by ignoring them. They’ll keep calling until you answer and move on to another person in your life, such as your family or friends. Additionally, many collectors have ways of tracking down people who don’t want to be found (it’s not always legal), so it’s better not to take any chances.

- Plan what you’ll say before you pick up the phone. Sometimes it helps to have a script prepared in advance so that when they ask why they haven’t received payment yet or what happened with their last check-in call, there won’t be a pause while you think about how best to respond; instead, there will only be time for them speak before answering questions yourself!

DON’T be coerced into making partial payments that you cannot afford.

- Don’t be coerced into making partial payments that you cannot afford. If a collector is pressuring you to make a payment, they are trying to get you to pay more than what is fair.

- Make sure that any payments made are affordable so that the debt will be settled within your means, rather than being added onto and continuing to grow as time passes (and interest accrues).

Feel free to ask the company to send you a breakdown of the amounts outstanding, including interest and penalties, if any.

If you’re having trouble paying a bill, it’s okay to ask the company for more information about what you owe. You can ask for an itemized breakdown of all charges and interest, if applicable. This way, you’ll know what exactly is going on with your debt and how much money is outstanding.

If there are additional charges that have been added to your bill (such as late or missed payment fees), these should also be included in the breakdown.

You may ask for a written notice of the debt and evidence that the creditor is the rightful owner of the debt.

- You may ask for a written notice of the debt and evidence that the creditor is the rightful owner of the debt.

- You should not pay a bill until you receive a written notice of the debt and evidence that the creditor is the rightful owner of the debt.

BE VERY CAREFUL and suspicious of any collection agency asking to “verify your personal information”.

You should be very careful and suspicious when a collection agency asks to “verify your personal information”, especially if they are asking for the following:

- Your date of birth.

- Your social insurance number.

- Any other identification numbers (like driver’s license numbers).

These types of questions are frequently used by criminals to steal your identity. If this happens to you, contact the police immediately and report the situation to them as well as contact Equifax Canada immediately at 1-866 828-5961 or report it on their website at https://www.equifax.ca 1-800-465-7166. After making a language selection, say “fraud” or press 3

Do not offer personal identification information or make any payment until you are certain the agency is legitimate.

DO NOT:

- give out personal information, including your address and phone number.

- make any payments or authorize a payment to the agency without first verifying its legitimacy.

- give out credit card or bank account information.

Many agencies are NOT willing to negotiate repayment plans that you can afford.

If you are in a situation where you are unable to pay back the full amount of your debt, there are options available to help you get on track. Many agencies are NOT willing to negotiate repayment plans that you can afford. However, some will work with their clients and may accept partial payments based on income or other factors.

The collection agency may be willing to negotiate repayment terms if they feel it is in their best interest or if they have been getting paid too little for too long (depending on how much time has passed). If this does not work out, then there may still be hope by contacting the creditor directly.

If speaking with the creditor doesn’t resolve things either, then it’s time for legal action! You should always seek legal advice before proceeding with any type of lawsuit against anyone or any entity because it could end up costing thousands more than originally expected just due solely to court costs alone without even considering lawyer fees yet!

You may prefer to propose a repayment plan in writing that you know you can afford and get them to agree in writing BEFORE you pay anything.

You may prefer to propose a repayment plan in writing that you know you can afford and get them to agree in writing BEFORE you pay anything. You can also request that they send proof of your debt, such as an invoice or statement, as this will help verify their claim. If they refuse to do so, it’s likely that they are not legitimate and should be ignored.

If you are not satisfied with their response, consider filing a complaint with your provincial regulator.

If you are not satisfied with the collector’s response and think that your consumer rights have been violated, consider filing a complaint with your provincial regulator. The provincial regulators are responsible for enforcing consumer protection laws in Canada and can investigate allegations of unfair practices and unlawful conduct on behalf of consumers. Many provincial regulators also provide information about how to file a complaint online or over the phone. For more information about how to file a complaint, visit the Office of the Privacy Commissioner website at https://www.priv.gc.ca/en/

Collection agencies must follow strict rules when collecting unpaid bills from individuals in Canada

- Collection agencies must be registered with the government.

- Collection agencies must follow certain rules when collecting unpaid bills from individuals in Canada.

- Collection agencies must follow the laws of the province in which they are registered. For example, a collection agency based in Ontario must abide by all of Ontario’s consumer protection laws, including those that require collection agencies to provide written notice before contacting you (except where they have no choice but to contact you).

Conclusion

At the end of the day, if you want to deal with bill collectors in Canada, it’s best not to ignore them. The only way that an agency can legally collect money from you is by using their collection process and following the rules laid out by provincial regulators. In many cases, they will try whatever they can think of to get money from you, but ultimately this means that if they can’t reach an agreement on a payment plan then there isn’t much else left for them to do except give up trying to collect altogether or take legal action against you for repayment of all owed amounts plus interest and penalties.

For more information on how CCDR can help you reach out to us at 888-354-4706 from anywhere in Canada or visit us online at www.ccdr.ca

Choosing the right debt help provider

Introduction

If you’re struggling with debt, there are a lot of options out there for getting help. But which one is right for you? This article will help answer that question and walk you through how to choose the best debt help provider.

Choose the best debt help provider for you

It is important to choose a debt help provider that is accredited, independent, and transparent.

- Accredited: The first thing to look for when choosing a debt help provider is whether or not it’s accredited by the government. This can be found on the website of your chosen provider. If you don’t see any accreditation information on their site, that’s probably a red flag and you should look elsewhere for help with your debts.

- Independent: You want to make sure that your debt management company doesn’t have any ties with other financial institutions (e.g., banks). This means they are not owned or affiliated with any banks or credit card companies and cannot offer products like loans through them either because it could compromise their independence as an unbiased third party in between you and those who owe you money such as credit card companies or lenders whose loans haven’t been paid off yet due to insufficient funds being available at the time when payment was due.”

Consumer Proposal

Consumer proposals are a negotiated settlement—but this one happens outside the courtroom and is legally binding, so once it’s agreed upon by all parties (including you), it must be followed through on. However, while this can be helpful in getting out of debt, it does require approval from creditors and approval from courts. These types of negotiations generally tend to result in better repayment terms.

How to choose the right debt help provider

- Look for a provider that is accredited.

- Consider a local provider.

- Make sure the provider has ample experience in debt relief.

- Choose an affordable company with transparent pricing.

- Beware of companies that are not flexible or supportive when you have questions or concerns about your debt relief plan (or anything else).

Don’t settle for something that doesn’t help.

It is important to know that it is not always necessary to settle for the first debt help provider you come across. Take some time and do your research before signing up with any company or person offering their services as a debt consolidator, credit counselor or debt management plan provider.

You don’t want to sign up with someone who doesn’t have your best interests in mind, nor should you sign up with them if they don’t meet all of your needs and/or budget requirements.

Conclusion

We hope the information here has helped you to decide which debt help provider is best for your situation. Remember, there are many out there so do your research before making a decision and don’t settle for something that doesn’t help you achieve your goals! To find out more feel free to reach out to us.

Money Saving Tips for New Parents

Introduction

As a parent, you want to provide your child with the best of everything. But that can be hard on the budget! I get it: You’re tired and busy, and you don’t really have time to do much other than take care of your little ones. But if you want to save money when you have kids, these tips will help.

Be Honest About Your Finances

You and your partner need to sit down and have a conversation about your finances. Be honest with each other about what you can afford, what you spend, your financial goals and priorities, as well as your current financial situation.

If one of the two of you has more debt than the other or makes more money than the other, that doesn’t mean that person should be responsible for everything—you both have a say in how much debt is taken on or how much money is spent on baby-related expenses.

Make a Baby Budget

You’ll need to determine how much money you can afford to spend on your new baby. First and foremost, write down all of the expenses that you have already incurred for the birth of your child. These might include hospital costs, doctor’s fees, items purchased at Babies R Us (or Target or Walmart), and any other related items that you have already spent money on.

Next, make a list of expected expenses for the coming weeks or months as well as some possible unexpected expenses that may come up during this time period. The latter could include additional tests or treatment from doctors not covered by insurance such as physical therapy sessions if there are developmental delays; prescriptions for medications; additional appointments with specialists like neurologists or speech therapists; toys that aren’t included in your “starter kit”; gifts from relatives & friends who want to shower them with things…

After making these two lists, calculate how much money you still need left over in order to save up enough funds so that whatever happens will not cause financial stress later on down when bills start rolling in faster than ever before! This is where being organized helps immensely because now at least we know what needs doing first: planning out our future finances so they’re no longer just abstract concepts but rather tangible goals which can be accomplished through careful budgeting decisions made every day.”

Create a Savings Plan

To create a savings plan you will need to:

- Set a savings goal. This is the amount that you want to save in total, over time. It could be as small as $500 or as high as $5 million.

- Set up a savings plan for how you are going to achieve your goal. Set aside enough money each month so that by the end of it all, your savings account will be full and ready for whatever comes next (whether it’s college tuition payments or retirement).

- Decide on how long it will take before reaching your goal—anywhere from one year to 40 years!

Take Advantage of Freebies

As you are probably aware, there are a number of freebies available to new parents. If you don’t know where to look, here are some tips:

- Take advantage of freebies in your area. There are likely several organizations in your community that offer vouchers or discounts for new parents. For example, the March of Dimes has partnered with companies like Babies R Us and Toys R Us to provide exclusive discounts on select products.

- Take advantage of freebies for families with kids aged zero through six years old. These deals come from corporations such as Waffle House and McDonald’s who want nothing more than for your children—and you—to have a happy meal experience!

- Look out for other deals on items like clothing or diapers too! Your baby doesn’t need designer clothes but if someone gives them away at no cost then why not take advantage?

Save money when you have kids!

- Buy clothes second-hand. It’s a great way to save money, and you can find some really cute stuff!

- Buy at the right time of year. Winter clothes are usually cheaper during autumn, while summer clothing is cheaper in spring.

- Buy in bulk if it’s something you use frequently (like baby food), but only if you need a lot of it. Buying big tubs of baby food will save you money, but they also take up space that could be used for more important things like more diapers or bottles (or maybe just more room for yourself).

Conclusion

So, now you know some of the best money saving tips for new parents. The key is to get started right away and make a plan that works for your family. If you have any questions about how to save money with kids, feel free to contact us!

Debt Relief options in Canada

Introduction

Debt is a very common problem in Canada. It has become an epidemic that many people are dealing with on a daily basis. There are many ways to deal with your debt and we will help you decide which one works best for your situation.

Debt Consolidation

Debt consolidation is a great way to lower your monthly payments and get a lower interest rate. You can consolidate all your loans into one loan, which will help you pay off the debt faster. It’s important that you consolidate the right debts: personal loans, credit cards, and lines of credit should be consolidated into a low-interest card or line of credit because these are high-interest debts.

If you want to pay off your debt faster, then it may make sense for you to use debt consolidation as part of your strategy.

Bankruptcy

Bankruptcy is a legal process that allows you to get rid of your debts. It’s the last resort and should only be considered if other options have failed.

- What are the benefits of bankruptcy? It can relieve you from most or all of your debts.

- What are the drawbacks? It can have a negative impact on your credit score for up to 10 years after completing it. Additionally, during bankruptcy proceedings, creditors may try to recover money owed before they release any claims against you. This may mean additional costs and fees before the process is complete (and even afterwards). Finally, while bankruptcy itself doesn’t take very long—usually between 3-6 months—there will be some administrative steps required by both yourself and any creditors involved in order for everything to go smoothly (just like filing taxes).

Credit counselling

If you’re in a financial bind, credit counselling can help. Credit counsellors are trained professionals who can help you understand your options and make the best decisions for your personal financial situation. They’ll also provide advice on how to avoid future debt problems.

Credit counsellors are not:

- Debt management programs (DMPs). DMPs typically involve paying a company monthly fees in exchange for them negotiating with creditors on your behalf. While this may seem like a good way to deal with debt, it has its drawbacks—the most notable being that many DMPs charge extremely high fees and take 40% or more of what they collect from each creditor as commission, which means there’s less money left over for you after all the bills are paid off. In addition, by using one of these companies instead of negotiating directly with creditors yourself, chances increase that they won’t be able to get favourable terms—which could lead to further stress down the road when something goes wrong (like missed payments) because there’s no real relationship between you and your debt collector! Credit counselling is free; don’t waste money on unreliable services!

- Bankruptcy. If things get truly dire and bankruptcy seems like the only option left open before filing Chapter 7 or Chapter 13 bankruptcy papers then see our article What Is Bankruptcy? You might be surprised at how much better off financially speaking starting fresh under another name will pay off long term compared

Consumer proposal

A consumer proposal is a legal agreement between a debtor and their creditors. The debtor agrees to pay the creditors a fixed amount over a period of time, while the creditors agree to accept that payment and not pursue other legal action against you.

The proposal is filed with the courts, where it’s reviewed by an independent trustee who decides whether or not it should be accepted. If your proposal is accepted, interest on your debt will be reduced to 0%. The Balance owing is also reduced in most cases by up to 70%!

Coaching program

If you’re looking for a debt relief option that will help to improve your financial situation, coaching may be the right choice. Coaching programs offer support and guidance as you work towards getting out of debt by changing your spending habits, managing your money and making better choices with regard to purchases. These programs can also provide accountability, since coaches will often check in with their clients on a regular basis via phone calls or meetings.

Coaching is based on the idea that if you have someone to guide you through the process of achieving your goals, then it’s more likely to happen quickly and efficiently than if you were trying to do it alone. A coach can provide motivation when necessary and help keep things like motivation levels high by encouraging clients in their efforts towards reaching these goals. It also gives people who need extra encouragement or motivation an outlet for this sort of support without having to think about where else they might get it from (such as family members).

5 different services to help resolve debt issues, each one different in it’s own way. Please pick the one that is right for you.

We offer 5 different services to help resolve debt issues, each one different in it’s own way. Please pick the one that is right for you.

- Debt Consolidation: Debt consolidation is a process where multiple debts are combined into a single payment that is paid off over time. This process can be used with your current creditors or new ones (if they will accept), and can help lower the amount of interest you pay per month on your existing debts. It will not reduce the amount owed to creditors however, which means they will still require repayment even after this process has been completed successfully.

- Bankruptcy: Bankruptcy has been around as long as money itself but many people do not know what it actually entails so we have written an article explaining everything there is to know about filing bankruptcy in Canada if this option interests you! In short though, filing for bankruptcy allows individuals who are insolvent due to their inability to pay back debts due their financial situation with reasonable effort over a reasonable period of time (3 years) obtain relief from those obligations under certain circumstances such as unemployment or disability; financial hardship caused by illness; unforeseen life events such as divorce/separation etc…

Conclusion

We hope this article has helped you understand the different debt relief options available in Canada. If you have any questions or would like to talk about your personal situation, please contact our office at (888) 354-4706. If you are not ready to talk on the phone or in person Chat with Jennie at www.ccdr.ca We are here to help!

Budgeting for Canadians

Introduction

Budgeting is an essential tool for managing your money and achieving your goals. Whether you’re trying to save up for a big purchase, figure out how much debt you have, or just get a feel for where your monthly income goes, budgeting lets you see what’s happening with your money in real-time.

Budgeting: A Guide to Spending Money Wisely

Budgeting is the process of planning your income, expenses, and investments. It can help you achieve financial freedom and give you peace of mind about your future.

There are many ways to make a budget, but this guide will show you how to create a simple one that works for most Canadians.

A good budget has four components:

- Income – what money comes into your home each month?

- Expenses – what money goes out of your home each month?

- Savings – what do you save each month?

- Debt repayment schedule (optional) – how much do you need to pay off on credit cards or other loans every month

Real-Life Budgeting

Real-life budgeting is a lot of work. It is not easy. You will have to make sacrifices and be willing to give up things that you might like or want, but can’t afford. But if you follow these steps, you will be able to create a budget that works for your life—and stick with it!

How to Create a Financial Plan in 8 Steps

- Start with your goals. What do you want to accomplish?

- Identify your income and expenses. Write down all of the money that comes in, and what it goes to (rent, transportation, food). Then write down where it goes (mortgage or rent payment, car payment, utilities).

- Create a budget based on these factors. This will help you see where you’re spending most of your money so that you can make changes if needed.

- Set up savings plans for both short-term goals (like buying something special) as well as long-term goals like retirement or buying a house. Remember that having some savings in an emergency fund is important too! Create separate accounts for each type of savings plan so you don’t accidentally spend from an account meant only for short-term goals (and vice versa).

- Create debt repayment plans using whatever method works best for your situation: paying off debt by interest rate order (highest interest first), a snowballing method where debts are paid off starting with the smallest balances first – this way if there’s no progress made on any one debt then there will be progress made on another one which builds momentum; other methods such as Dave Ramsey’s “Debt Snowball” method may also work well depending on what kind of counselor/advisor services are available locally before committing fully

Benefits of Budgeting

Budgeting is a way of life that many Canadians can benefit from. Through budgeting, you will be able to plan better, save money and pay off debt. You can also achieve your financial goals and even get out of debt!

Becoming a budgeter allows you to save for retirement. This is important because it means that you won’t have to worry about money when it comes time for you to retire–you’ll already have it saved up! It also means that when retirement does come around, the amount of money available isn’t as much as they had originally thought they would have by now.

Creating a Budget

You need a budget. A budget is a tool to help you manage your money. It’s not a punishment, and it’s not a rigid rule that you have to follow blindly. Instead, think of it as a guideline that helps guide your financial decisions so they align with your long-term goals.

Budgets are often made up of several types of information: income (what you earn), expenses (what goes out), savings goals (money for the future), and investments (investments).

A budget is an essential tool for managing your money and achieving your goals.

A budget is an essential tool for managing your money and achieving your goals. A budget is a plan that helps you manage your money so that you can make sure you have enough money to cover all of your expenses.

Your goal might be saving up for a vacation, paying off debt, or buying a new car. Whatever it is, setting aside some of your income each month will help make this dream become reality.

Creating a budget doesn’t need to be complicated or stressful—it’s just about knowing how much you spend on different things each month and making sure those amounts don’t go over certain limits.

Here’s how it works:

Conclusion

Hopefully, we’ve convinced you of the benefits of budgeting and shown you how to get started. If you’re looking for more tips on how to manage your money, check out our other articles on this topic. We also have an article about saving money every month with a few simple tricks

How You Can Deal with Debt Collectors!

When you’re dealing with debt, one of the most stressful things can be the constant harassment from debt collectors via phone calls and letters. Fortunately, you do have some rights and protection as you deal with them.

Debt collectors are required to follow certain guidelines as they attempt to collect outstanding debts. They are different from Province to Province. For example, they can’t call before 8:00 am or after 9:00 pm.

There are a few ways to deal with debt collectors. The simplest is to simply not answer the call. If you have caller ID on your phone and don’t recognize who is calling, don’t answer. If it turns out to be somebody you would like to talk to, he or she can leave a message.

The most obvious and effective option for dealing with debt collectors is to actually pay the debt. After all, you agreed to pay the debt when you acquired it and you, therefore, should repay the creditor who lent you the money.

If you are unable to repay the debt in full at once for some reason, you may be able to negotiate a reduced interest rate or partial repayment if you explain your situation. Keep in mind, however, that telling a creditor you’ve run up the debt by doing too much unnecessary shopping is not going to gain you much sympathy. On the other hand, if you’ve just been fired from your job and are going through legitimately difficult financial times while you look for another, this will likely give you some room for negotiation.

If you do negotiate a better deal with your creditors, be sure to keep your word and pay what you’ve said you would. While bill collectors may seem relentlessly cruel, they’re really just there to collect the money you owe. That’s their job. Once you have made arrangements with creditors to repay what you owe them and have shown that you can be trusted to keep your word, bill collectors will move onto other people and leave you alone.

Alternatively if your are in a tight spot and need assistance beyond just paying the debt. Reach out to us and we would be glad to assist you in a debt rescue plan.

5 Facts You Must Know When Applying For a Loan

APPLYING FOR A SECURED LOAN WITH BAD CREDIT

Having bad credit history can be like carrying a backpack full of worries. You don’t only have to face the elevated rates on credit cards and loans, but acquiring any type of credit can seem like an unbearable obstacle to overcome. Some people with bad credit think that all odds are against them when trying to apply for credit or loans. However, there are those who are willing to take the plunge in risky waters for you provided that you pay them back in the end. Secured loans use an item of monetary value as a safe keep known as collateral. The information that follows has reference to requesting a secured loan with w/unfavorable credit.

SECURED LOANS

Secured loans use personal property to secure the repayment of a loan. This means that the possibilities of getting a secured loan with bad credit are much higher than an unsecured loan. Their characteristics are that of being much more common and have lower interest rates. The interest rate that accompanies a secured loan depends on the value of the collateral being used and its´ place in the stock exchange should the lender have to sell it.

COLLATERAL

A kaleidoscope of items can be used as collateral for a secured loan. But those that have a higher monetary value than the loan amount itself tend to be the best collateral. Some items that are purchased with loans serve as their own collateral as in the case with a mortgage and automotive loans. Nonmaterial collateral such as capital built up in real estate often fulfills the duties for better collateral for a secured loan than any other item.

SHOPPING FOR A LOAN

It’s just as important to look around for a secured loan as it is to get a second opinion from a doctor. When shopping around for a secured loan, the following suggestions should never be overlooked. *Take the time to investigate different banks, finance companies, and lenders in your area who offer the best interest rates or loans. *Online lenders which can often feature better interest rates *Once you have all the information, make comparisons to see which loan suits you the best.

APPLYING FOR YOUR LOAN

Once you’ve found your loan, the application must be submitted. Even though a great-looking shoe doesn’t always secure a perfect fit, it’s essential to have other proposals at hand. If all fails and you still haven’t found your match, it may be time to expand your horizons & undertake other options to facilitate the quest for the best loan that suits your needs.

Consolidating credit card debt

Is consolidating credit card debt a good option?

Well, the answer will more often be yes than no. Consolidating credit card debt is often regarded as the first step towards credit card debt elimination. However, even before you move to take the first step towards consolidating credit card debt, you must understand that consolidating credit card debt (or balance transfer) is an action that you are taking to eliminate credit card debt. Consolidating credit card debt is not a means of deferring the problem for later.

Consolidating credit card debt is indeed a good option in more than one sense. Not only do you get relief from the rapid increase in your credit card debt, but you also get other benefits too. Offers for consolidating credit card debt are in abundance and are very attractive indeed. Almost all the offers for consolidating credit card debt have an initial low APR period during which the APR is generally 0% (or some low figure). This is one of the main things that make consolidating credit card debt a desirable option. Besides this low APR, the offers for consolidating credit card debt also include no interest rate on the purchases made during the first 5 months (or some other initial period) of the balance transfer. This is another thing that lowers the speed at which your credit card debt gallops. These are the two most important benefits that credit card suppliers deploy to attract people into consolidating credit card debt with them. There are other benefits, which include things like additional reward points on the member’s reward program of the credit card you are consolidating credit card debt to. These reward points can be redeemed for other attractive goods/rebates/rewards etc. Sometimes, the new credit card (i.e., the one you are consolidating credit card debt to) might be a credit card that caters more to your current spending needs regarding the credit limits and the way you spend your money. For example, the new credit card might be a co-branded one offered by an airline that you have started traveling with very frequently in recent times, and consolidating credit card debt on such a card may open up much more benefits as compared to your current credit card which was based on your needs at the time of you applying for your current credit card. The credit card you are consolidating credit card debt to might open up discount offers to you.