Budgeting

Back to School Budgeting: Smart Strategies for a Smooth Start

Are you ready for the upcoming school year? As the back-to-school season approaches, it’s essential to prepare your child and your budget. Balancing the costs of supplies, clothing, and other necessities can be daunting, but with the right strategies, you can ensure a smooth and stress-free transition. In this article, we’ll explore practical ways to budget for the back-to-school season while keeping your finances in check.

Creating a Comprehensive Back-to-School Budget

- Assess Your Needs and Prioritize Before embarking on your back-to-school shopping journey, take some time to assess your needs. List essential items such as school supplies, uniforms, backpacks, and electronics. Prioritize these items based on their urgency and importance. This step will help you allocate your budget more effectively.

- Set a Realistic Spending Limit. Determine how much you can comfortably spend on back-to-school expenses without straining your finances. Consider your overall financial situation, including income and other financial commitments. Setting a spending limit will prevent overspending and ensure you stay within your means.

- Research and Compare Prices Take advantage of online resources and local store flyers to research and compare prices for different items. Look for sales, discounts, and special offers that can help you save money. Remember, a little extra effort in comparing prices can lead to significant savings in the long run.

- Involve Your Children Include your children in the budgeting process. Discuss the budget constraints with them and encourage them to make thoughtful decisions when selecting items. This teaches them about financial responsibility and helps them understand the value of money.

Smart Shopping Strategies

- Shop Early and Spread Out Purchases Avoid the last-minute rush by starting your shopping early. You can use different sales and deals by spreading your purchases over a few weeks. This approach also allows you to avoid impulse buying, which can lead to unnecessary expenses.

- Buy Secondhand When Possible Consider purchasing secondhand items such as textbooks, clothing, and electronics. Online platforms and thrift stores often have gently used items at a fraction of the cost. Just be sure to inspect the items for quality before making a purchase.

- Utilize Coupons and Cashback Offers. Clip coupons from newspapers or digital coupon apps to save on various items. Additionally, consider using cashback websites or credit cards that offer cashback rewards on back-to-school purchases. Every little bit of savings adds up!

Transitioning Back to School Smoothly

- Prepare Meals at Home Packing lunches and snacks at home can help you save a significant amount of money compared to buying from school cafeterias or fast-food establishments. Plan nutritious and budget-friendly meals that your child will enjoy.

- Explore Free or Low-Cost Activities Instead of spending money on costly after-school programs or entertainment, explore free or low-cost activities in your community. Libraries, parks, and community centers often offer educational and recreational options for children.

- Encourage Open Communication Keep the lines of communication open with your child about budgeting and spending. Discuss the importance of making responsible choices and the value of money. By fostering these conversations, you empower your child to develop strong financial habits from a young age.

Navigating the back-to-school season with a well-structured budget is a prudent approach that benefits your finances and your child’s education. You can make the most of this exciting time by assessing your needs, setting limits, and employing savvy shopping strategies without breaking the bank. Remember, careful planning and thoughtful spending will ensure a successful transition back to school while keeping your financial goals intact.

Exploring Canada’s Prime Interest Rate: A Key Indicator of Economic Stability

The prime interest rate is a crucial benchmark that significantly shapes Canada’s financial landscape. As a critical monetary policy tool, it influences borrowing costs, impacts the housing market, and reflects the overall state of the economy. In this article, we will delve into the prime interest rate in Canada, its importance, and how it affects various aspects of our daily lives.

Understanding the Prime Interest Rate: The prime interest rate represents the interest rate banks charge their most creditworthy customers for loans. It serves as the foundation for determining borrowing costs across various financial products, including mortgages, personal loans, business loans, and lines of credit. The Bank of Canada sets the target for the prime rate, which influences lending rates across the country.

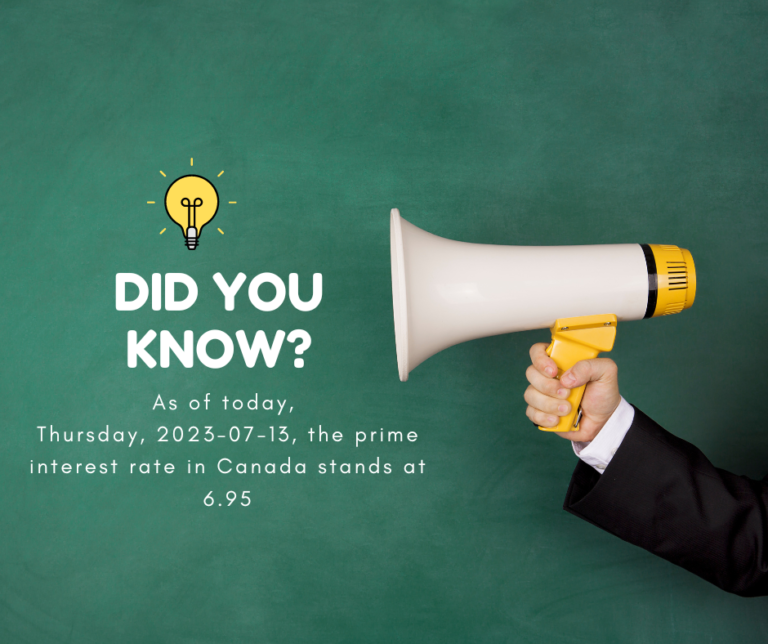

Current Prime Interest Rate in Canada: As of today, Thursday, 2023-07-13, the prime interest rate in Canada stands at 6.95%. It is important to note that the prime rate can fluctuate over time as economic conditions change. Financial institutions may adjust their prime rates accordingly, reflecting factors such as inflation, economic growth, and the monetary policy decisions of the central bank.

Impact on Borrowers: The prime interest rate directly affects borrowers in Canada. When the prime rate increases, borrowing costs rise, making it more expensive to take out loans or carry balances on lines of credit. Conversely, decreasing the prime rate can lead to lower borrowing costs, providing potential savings for borrowers. Homeowners with variable-rate mortgages are particularly impacted, as their interest rates can change when the prime rate fluctuates.

Influence on the Housing Market: The prime interest rate significantly influences the housing market. When the prime rate is high, mortgage rates tend to increase, making it more challenging for prospective homebuyers to afford homeownership. Conversely, a lower prime rate can stimulate the housing market by making mortgages more affordable and potentially increasing property demand. It is essential for individuals considering homeownership to monitor changes in the prime rate to make informed decisions.

Economic Indicator: The prime interest rate is also a crucial economic indicator. It reflects the central bank’s assessment of the country’s economic conditions and efforts to manage inflation and stimulate economic growth. When the prime rate is adjusted, it can signal the central bank’s stance on monetary policy and its views on the economy’s overall health.

The prime interest rate is a vital element of Canada’s financial system, influencing borrowing costs and reflecting the state of the economy. As of today, the prime rate in Canada stands at 6.95%. Understanding the prime rate’s impact on borrowing costs, the housing market, and its role as an economic indicator helps individuals make informed financial decisions. Keeping a close eye on changes in the prime rate can help borrowers and potential homeowners navigate the ever-changing financial landscape.

10 Tips for Maintaining a Healthy Budget at Home

Maintaining a healthy budget at home has become more critical today, where everything seems to be getting expensive daily. As a result, we have to be more mindful of our finances and keep our expenses in check. This article will provide ten practical tips for maintaining a healthy budget at home.

Create a budget plan

Creating a budget plan is the first step in maintaining a healthy home budget. This will help you keep track of your expenses and identify areas where you can cut down your costs. Next, list your monthly income and expenses, including your bills, groceries, and other miscellaneous costs.

Cut down on unnecessary expenses

Once you have created your budget plan, it’s time to cut down on unnecessary expenses. This includes dining out, buying clothes you don’t need, and subscription services you rarely use. Instead, focus on spending on essential items and prioritize your expenses accordingly.

Plan your meals in advance

Planning your meals can help you save significant money. For example, list the groceries you need for the week and avoid impulse purchases. Additionally, you can opt for budget-friendly meals and make use of leftovers.

Avoid unnecessary debt

Avoid taking on unnecessary debt and always pay your bills on time. This will help you avoid late fees and penalties, which can add up to a significant amount over time. In addition, if you have existing debt, pay it off as soon as possible to avoid accruing additional interest charges.

Reduce energy consumption

Reducing your energy consumption can help you save significant money on your utility bills. You can do this by turning off lights and appliances when not in use, using energy-efficient light bulbs, and reducing water usage.

Consider refinancing your mortgage

If you have a mortgage, consider refinancing it to a lower interest rate. This can help you save on monthly mortgage payments and free up extra cash for other expenses.

Find ways to earn extra income

Finding ways to earn extra income can also help you maintain a healthy budget at home. For example, you can take on a part-time or freelancing job, sell unwanted items online, or offer your skills and services to others.

Use coupons and discount codes

Using coupons and discount codes can help you save money on your purchases. Look for online deals and coupon codes before purchasing, and take advantage of sales and promotional offers.

Invest in home maintenance

Investing in home maintenance can help you avoid costly repairs and replacements in the future. Regularly cleaning and maintaining your home appliances and systems can also help you save money on your utility bills.

Set financial goals

Finally, setting financial goals can help you stay motivated and focused on maintaining a healthy budget at home. Whether saving for a vacation or paying off debt, having a clear plan can help you prioritize your expenses and make smart financial decisions.

In conclusion, maintaining a healthy budget at home requires discipline, planning, and intelligent financial decisions. By following these tips, you can reduce your expenses, avoid unnecessary debt, and save money for the future.

2023 Money-Saving Hacks for Frugal Living

-

Table of Contents

“2023: Unlock the Secrets to Frugal Living and Save Money Now!”

Introduction

Are you looking for ways to save money in 2023? With the cost of living on the rise, it’s important to find ways to save money and live frugally. Fortunately, there are plenty of money-saving hacks that can help you stretch your budget and make the most of your money. In this article, we’ll share 2023 money-saving hacks for frugal living that can help you save money and live a more financially secure life. From budgeting tips to smart shopping strategies, these hacks will help you make the most of your money and live a more frugal lifestyle.

10 Energy-Saving Tips for Sustainable Living in 2023

1. Invest in energy-efficient appliances: In 2023, energy-efficient appliances will be more affordable and widely available. Look for appliances with the Energy Star label, which indicates that they meet the highest standards for energy efficiency.

2. Install solar panels: Solar panels are becoming increasingly popular and cost-effective. Installing solar panels on your roof can help you save money on your energy bills and reduce your carbon footprint.

3. Use LED light bulbs: LED light bulbs are more energy-efficient than traditional incandescent bulbs. They also last longer, so you won’t have to replace them as often.

4. Unplug electronics when not in use: Even when electronics are turned off, they can still draw power. Unplugging electronics when not in use can help you save energy and money.

5. Install a programmable thermostat: Programmable thermostats allow you to set different temperatures for different times of the day. This can help you save energy by only heating or cooling your home when you need it.

6. Insulate your home: Proper insulation can help keep your home warm in the winter and cool in the summer. This can help you save energy and money on your energy bills.

7. Use natural light: Natural light is free and can help you save energy. Open your curtains and blinds during the day to let in natural light and reduce your need for artificial lighting.

8. Plant trees: Trees can help reduce energy costs by providing shade and blocking wind. Planting trees around your home can help you save energy and money.

9. Use a clothesline: Instead of using a dryer, hang your clothes on a clothesline to dry. This can help you save energy and money on your energy bills.

10. Buy local: Buying local products can help reduce your carbon footprint. Look for locally-sourced food and other products to help reduce your energy consumption.

10 Smart Spending Strategies for Frugal Living in 2023

1. Make a budget and stick to it: The most important step to living frugally is to create a budget and stick to it. This will help you stay on track with your spending and ensure that you are not overspending.

2. Shop around for the best deals: Don’t just settle for the first price you see. Take the time to shop around and compare prices to get the best deal.

3. Buy in bulk: Buying in bulk can save you money in the long run. Look for bulk discounts and stock up on items that you use regularly.

4. Use coupons and discounts: Coupons and discounts can help you save money on everyday items. Take the time to look for coupons and discounts before you make a purchase.

5. Buy used items: Buying used items can save you a lot of money. Look for second-hand stores or online marketplaces to find great deals.

6. Make your own meals: Eating out can be expensive. Instead, try making your own meals at home. This will save you money and you can control the ingredients you use.

7. Cut back on entertainment expenses: Entertainment expenses can add up quickly. Try to find free or low-cost activities to do instead of spending money on expensive entertainment.

8. Take advantage of free services: There are many free services available online that can help you save money. Take advantage of these services to save money on things like streaming services, online courses, and more.

9. Use cash instead of credit cards: Credit cards can be tempting, but they can also lead to overspending. Try to use cash instead to help you stay on budget.

10. Invest in yourself: Investing in yourself can help you save money in the long run. Take the time to learn new skills or take classes that can help you advance in your career. This can help you earn more money and save more in the future.

10 Simple Living Tips for Financial Planning in 2023

1. Make a budget and stick to it. Start by tracking your spending for a month and then create a budget that works for you. Make sure to include savings in your budget.

2. Pay off debt. Paying off debt is one of the best ways to improve your financial situation. Make a plan to pay off your debt as quickly as possible.

3. Automate your savings. Set up automatic transfers from your checking account to your savings account each month. This will help you save without having to think about it.

4. Invest in yourself. Investing in yourself is one of the best investments you can make. Invest in your education, skills, and career to increase your earning potential.

5. Live below your means. Don’t buy things you don’t need and don’t spend more than you make. Live within your means and save the rest.

6. Take advantage of tax breaks. Make sure you’re taking advantage of all the tax breaks available to you. This can help you save money and reduce your tax bill.

7. Start a side hustle. Consider starting a side hustle to increase your income. This can be anything from freelancing to selling items online.

8. Build an emergency fund. An emergency fund is essential for financial security. Aim to save at least three to six months of living expenses in an emergency fund.

9. Take advantage of employer benefits. Many employers offer benefits such as retirement plans and health insurance. Make sure you’re taking advantage of these benefits to save money.

10. Get professional advice. If you’re feeling overwhelmed by your finances, consider getting professional advice from a financial planner or accountant. They can help you create a plan to reach your financial goals.

10 DIY Solutions for Cost-Cutting in 2023

1. Invest in Automation: Automation can help reduce costs by streamlining processes and eliminating manual labor. Investing in automation can help you save money in the long run.

2. Outsourcing Non-Core Tasks: Outsourcing non-core tasks can help you save money by allowing you to focus on core tasks and reduce overhead costs.

3. Leverage Cloud Computing: Cloud computing can help you reduce costs by eliminating the need for expensive hardware and software.

4. Utilize Open Source Software: Open source software can help you save money by eliminating the need to purchase expensive software licenses.

5. Negotiate Better Deals: Negotiating better deals with suppliers and vendors can help you save money by getting better prices for the same products and services.

6. Reduce Energy Consumption: Reducing energy consumption can help you save money by reducing your energy bills.

7. Invest in Employee Training: Investing in employee training can help you save money by increasing employee productivity and reducing turnover.

8. Implement Lean Manufacturing: Lean manufacturing can help you reduce costs by eliminating waste and increasing efficiency.

9. Utilize Data Analytics: Data analytics can help you save money by providing insights into customer behavior and trends.

10. Invest in Cybersecurity: Investing in cybersecurity can help you save money by preventing data breaches and other cyber threats.

10 Creative Ways to Save Money on Groceries in 2023

1. Take advantage of store loyalty programs. Many grocery stores offer loyalty programs that can help you save money on groceries. Look for discounts, coupons, and other special offers that you can use to save money.

2. Buy in bulk. Buying in bulk can help you save money on groceries. Look for items that you use often and buy them in larger quantities. This can help you save money in the long run.

3. Shop at discount stores. Discount stores like Aldi and Lidl offer great deals on groceries. You can often find items for much cheaper than you would at a regular grocery store.

4. Buy generic brands. Generic brands are often much cheaper than name brands. Look for generic versions of items that you use often and save money.

5. Use coupons. Coupons are a great way to save money on groceries. Look for coupons in the newspaper, online, or in-store circulars.

6. Buy in season. Fruits and vegetables that are in season are often much cheaper than those that are out of season. Look for seasonal produce and save money.

7. Buy frozen. Frozen fruits and vegetables are often much cheaper than fresh ones. Look for frozen versions of items that you use often and save money.

8. Buy store brands. Store brands are often much cheaper than name brands. Look for store brands of items that you use often and save money.

9. Buy in bulk online. Buying in bulk online can help you save money on groceries. Look for online stores that offer bulk discounts and save money.

10. Meal plan. Meal planning can help you save money on groceries. Plan out your meals for the week and buy only what you need. This can help you save money and reduce food waste.

Conclusion

2023 Money-Saving Hacks for Frugal Living is a great way to save money and live a more frugal lifestyle. By taking advantage of the various money-saving hacks, you can save money on everyday expenses, such as groceries, utilities, and entertainment. Additionally, you can save money on larger purchases, such as cars and vacations. With a little bit of effort and creativity, you can make the most of your money and live a more frugal lifestyle.

Budget and Pay off Debt Simultaneously

5 Steps to Budgeting and Paying off Debt

Debt can be a heavy burden, but with proper planning and by following these five steps, managing finances and reducing debt can become a reality. A comprehensive budgeting strategy is key to prioritizing expenses, saving money, and quickly paying off debt.

Step 1: Evaluate Finances

Initially, it is important to gain a clear understanding of your current financial situation. This involves calculating your monthly income and expenses, including any existing debt. By identifying areas to reduce expenses, you can allocate more funds towards debt repayment.

Step 2: Draft a Budget

After evaluating your finances, the next step is to create a budget that suits your needs. This budget should include all necessary expenses such as housing, utilities, food, transportation, and entertainment. Above all, it is crucial to make debt repayment a top priority in the budget.

Step 3: Focus on Debt Repayment

To make the most of your budget and reduce debt effectively, it’s essential to target the debt with the highest interest rate first. By doing so, you’ll save money on interest and speed up the debt elimination process. Once one debt is paid off, you can redirect the payments towards the next debt on your list.

Step 4: Monitor Progress

As you make progress, it’s important to frequently review your budget and make any necessary adjustments. Seeing tangible progress towards your financial goals can be a great source of motivation and help you stay on track.

Step 5: Celebrate Success

Finally, it’s crucial to acknowledge and reward your hard work. Whether it’s paying off a debt or reaching a savings goal, take time to celebrate your success and recognize your efforts.

Balancing debt and budgeting can be a challenging task, but by following these five steps, you can take control of your finances, reduce debt, and reach your financial goals.

Why its important to track your spending

Tracking your spending is an essential step in taking control of your finances. It allows you to see where your money is going, identify areas where you may be overspending, and make adjustments to your budget accordingly.

One of the biggest benefits of tracking your spending is that it helps you to create and stick to a budget. When you know exactly where your money is going, you can make informed decisions about where to allocate funds and where to cut back. This can help you to save money and reach your financial goals more quickly.

Tracking your spending also allows you to identify areas where you may be overspending. For example, you may realize that you are spending too much on dining out or entertainment. Once you identify these areas, you can make changes to your spending habits and redirect that money to more important things like saving for retirement or paying off debt.

Additionally, tracking your spending can also help you to spot any suspicious activity on your bank account. If you notice any unauthorized charges, you can quickly report them to your bank or credit card issuer and take steps to protect your financial information.

Overall, tracking your spending is an essential step in managing your finances effectively. It allows you to create a budget, identify areas of overspending, and take control of your money. By keeping a close eye on your spending, you can make sure that your money is being used in the way that you want it to be, and reach your financial goals more quickly.

Its 2023 Time to Make a budget!

Creating a budget is an important step towards financial stability and security. By tracking your income and expenses, you can make sure that you are saving enough money and not overspending. Here are some steps to help you create a budget:

- Gather your financial information. This includes your income (e.g. salary, investments, etc.), expenses (e.g. rent, utilities, groceries, etc.), and debts (e.g. student loans, credit card balances, etc.).

- Calculate your net income. This is the amount of money you have left after deducting taxes and other deductions from your gross income.

- Make a list of your fixed expenses. These are expenses that remain the same each month, such as rent or a mortgage payment, car payment, and insurance premiums.

- Identify your variable expenses. These are expenses that can fluctuate from month to month, such as groceries, entertainment, and dining out.

- Determine your savings goals. This could include saving for a down payment on a house, building up an emergency fund, or saving for retirement.

- Compare your net income to your expenses. If your expenses are more than your income, you will need to find ways to cut back on your spending or increase your income. If you have money left over after paying your expenses, you can allocate it towards your savings goals.

- Create a budget plan. This can be as simple as a list of your expenses and how much you plan to spend on each one. Or, you can use a budgeting app or spreadsheet to track your spending and see how you are doing against your budget.

- Review and adjust your budget regularly. As your income and expenses change, it’s important to update your budget to reflect these changes. By reviewing your budget regularly, you can make sure that you are staying on track and making progress towards your financial goals.

Creating a budget takes some time and effort, but it is a valuable tool for managing your money and achieving your financial goals. By tracking your income and expenses and making informed decisions about how you spend your money, you can take control of your finances and build a solid foundation for your future.

Why it is Important to Avoid Debt

Debt is a necessary part of life. You need to borrow money in order to buy a house, start a business or go on vacation. However, it’s important that you avoid debt whenever possible. There are many reasons why you should avoid becoming too dependent on debt and some of them include:

Debt does not go away by itself

Debt is a long-term problem, and it won’t just go away.

It’s important to understand that debt doesn’t disappear on its own. There are many people who think they can just ignore their debt and it will eventually go away, but this isn’t true at all! The only way for your debt to truly disappear is if you take action. If you don’t take action, then your situation will continue to get worse until you start having problems with your finances and other areas of life as well.

Debt affects more than just your finances; it also affects your emotions.

Remember: Debt isn’t just a financial problem; it also has emotional consequences as well. As far as mental health goes, dealing with debt can be very stressful and exhausting—and sometimes even downright depressing! However if one approaches their situation with positivity instead of negativity (i.e., says something like “I’m going through a tough time right now but I know things will turn around soon”) then they’ll end up feeling much better about themselves by staying positive despite all odds stacked against them today or tomorrow…or whenever else they might encounter problems caused by someone else’s mistake (in this case being responsible enough not only pay off all debts owed but also never get into any kind of trouble again).

Debt can lead to bankruptcy and foreclosure.

While it may sound extreme, bankruptcy and foreclosure are a reality for many Canadians. Bankruptcy is a legal process that allows you to deal with debt, while foreclosure is the legal process of dealing with debt by selling your house to pay off any outstanding loans.

Regardless of the type of debt you have, both processes can be avoided if you are proactive in taking care of things before they get out of hand.

Debt carries hidden fees that you may not be aware of.

Hidden fees are charges that you didn’t know about at the time of signing. Hidden fees can be charged by lenders or credit card companies and can include interest rates, transaction fees, annual fees and late payment penalties. If you are not aware of these fees it may be difficult to budget for them or plan ways to avoid paying them in the future.

In addition to being a financial burden, debt can negatively affect your emotional well-being.

In addition to being a financial burden, debt can negatively affect your emotional well-being.

You may not realize that your finances are making you anxious, depressed or even suicidal until it’s too late. Be aware of the following signs:

- You feel like you’re drowning in debt. If this is how you feel, it may be time to seek help from someone who can assist you with gaining control over your finances once again.

- Your relationships are suffering because of money issues. For example, if you are unable to pay for necessities such as rent and utilities without asking friends or family members for help, it could lead them to resent having to take care of an adult who is “wasting money on frivolous things.”

Problems with debt can cause severe financial problems.

In addition to the obvious costs incurred from paying interest on a debt, there is a host of other problems that can arise from taking on debt. For example, having too much debt can affect your credit score and ability to get a loan. If you have too many loans or high balances on your accounts, it can make it difficult for lenders to determine whether or not they should trust you with a new loan or credit card. Even worse, if you have no money in savings and few assets besides whatever assets are already secured by mortgages or car loans (like a house or car), then there may be nothing available for lenders to take if they need to foreclose on their collateralized property.

In addition to potentially hurting your ability to purchase property or buy things like cars in the future (due to negative equity), taking out too much debt could also prevent people from buying those important things now due simply because they don’t have enough income left over after paying bills each month! This means that even though someone might really want something nice like an iPhone X but know full well that making payments every month will mean less money left over at month’s end so only having enough money after all bills are paid each month – then maybe buying one isn’t worth doing at this point because then where does one find funds for food/rent/etcetera?”

Avoiding debt is so important because it causes emotional pain and financial hardship.

So, why is it important to avoid debt? The answer is simple: debt can cause emotional pain and financial hardship.

When you are in a lot of debt, or when you have a high credit card balance, it can be stressful. You might become anxious about not being able to make ends meet each month and worry about where the money for your bills is going to come from.

This stress can lead to depression if it continues for too long. It’s also common for people who are struggling financially due to their debt problems not only feel stressed but also anxious and depressed as well as angry with themselves or others around them who caused them these problems like their spouse or close friends/family members who aren’t helping understand what they feel like when they see each other at work because they know how much money we owe every month which makes things worse because there’s nothing anyone else could do right now except let me know that everything’s going ok?”

Conclusion

We hope this article has helped you understand why it is important not to get into debt. If you are suffering from debt, we would like to encourage you to seek help from a financial advisor or credit counselor. They will be able to help you with your situation and make sure that your future finances stay on track!

Back to School in Canada on a budget in 2023

The back-to-school season is upon us, and that means it’s time to stock up on all the supplies you’ll need for your kids to get back into the swing of things. But if you’re like me, that can mean spending hundreds of dollars on basic items like notebooks and pencils — all while living in an expensive city where rent keeps going up. So how do parents who want their kids to get a great education without breaking the bank manage? Here are some tips that might help:

Take inventory of your supplies

The first thing you will have to do is take inventory of your supplies. Do you have everything that is going to be necessary for the school year? Are there any items that you need to buy or borrow from someone else? If so, make a list of these things so that it’s easier for you and your family members when shopping for them.

Once this step is done, organize them in a way that makes sense for you. For example: if all of your pencils are in one place and all of your notebooks are in another place, then keep them separated by color as well (blue pencils with blue notebooks). This way they’ll be easier to find when needed! If some students prefer using pens over pencils, then let them use their own method but still keep track of which item belongs where by labeling each one accordingly (e.g., “This is my pen.”/”This belongs here”). Remember not only does organization make things easier but also helps prevent losing anything important like keys or electronics during class time!!

Make a list and budget

Now that you’ve got a general idea of how much money to expect and where to find it, it’s time to make a list and budget.

First, make a list of everything you need for school. These could include:

- Textbooks

- School supplies (like pencils, paper, binders)

- Lunch money or snacks

Look for deals and coupons

- Check newspapers and magazines. Many newspapers have a section of coupons, so you can look for them every week at your local grocery store.

- Check online coupon sites. Websites like Groupon and Living Social are great places to find deals on everything from restaurants to beauty treatments to school supplies. If there’s a deal for anything that you need for back-to-school, it’s probably on one of these sites!

- Look for coupons on social media. It’s pretty common nowadays for companies to offer coupons through their social media channels—so if you see any companies that sell the types of things in which you’re interested (e., pens or notebooks), make sure to follow them so that they can keep you up-to-date with new offers as they come up!

- Look in store flyers: Many stores will send out flyers with all sorts of special offers in them! Keep an eye out for any sales or discounts that might be available during back-to-school season at stores like Staples and Walmart; often times these stores will have big sales right around August when kids start school again after summer vacation ends (this also works great since most schools start around September/October).

Conclusion

We hope that you have found our tips on back to school in Canada on a budget useful. While it can be expensive, there are plenty of ways to save money and still find everything you need for school. You just have to know where to look!

How Much Money do you need for retirement in Canada?

Retirement is something that few people think about in their 20s and 30s and a large segment of the population around 50 isn’t really sure what they need to do to fund their retirement years. While there are many variables that come into play, one way is to figure out approximately how much money you will need in retirement. A good rule of thumb is this: in today’s dollars, you will need a minimum $1 million dollars to comfortably retire in Canada. To get to $1 million at retirement, assuming you make $50,000 per year, you should try to save at least 15% per year (if you start in your early 20s); if you start later, say in your 30s, try saving closer to 20%. If it’s still early enough for you (say under 40), then saving closer to 25-30% per year would be better!

Retirement is something that few people think about in their 20s and 30s and a large segment of the population around 50 isn’t really sure what they need to do to fund their retirement years.

It’s important to remember that retirement is a long way off for most people. At this point in your life, you’re probably thinking about getting through the next day, let alone planning for retirement. But if it’s not on your radar yet, it will be soon. You’ll find yourself thinking about saving money with every paycheck or maybe even setting up an automatic transfer from your checking account into a savings account when each paycheck hits.

The earlier you start saving money for your future self (retirement), the more time it has to grow and compound into something significant by the time you retire. If you wait until later in life to start saving for retirement without any previous contributions, then expect to have less money at that time—which means fewer options available to help fund those years when they come around! So while there aren’t any hard deadlines or cutoff dates where once passed there’s no going back (unless we’re talking about investing in crypto-currencies here), there are definitely advantages if done sooner rather than later.

While there are many variables that come into play, one way is to figure out approximately how much money you will need in retirement.

While there are many variables that come into play, one way is to figure out approximately how much money you will need in retirement.

In order to determine this, you will need to know what your living expenses will be once you stop working full-time. This includes housing costs and utility bills as well as any medical expenses that may arise. You should also consider transportation costs if you plan on continuing with a car payment or other regular expenses such as insurance premiums or memberships for sports clubs or gyms (if applicable).

Once you have an idea of how much money is necessary for each month in retirement, multiply it by the number of months per year (12) and then divide by 12 again to get an annual amount needed per month:

A good rule of thumb is this: in today’s dollars, you will need a minimum $1 million dollars to comfortably retire in Canada.

The rule of thumb is to save 15-20% of your income. The more you can save, the less likely you will need to worry about how much money do I need for retirement in Canada. If you are saving this amount every month, even if it’s small, then it adds up over time. You should also think about investing that money in ways that will grow and eventually make enough interest so that you can live off of the investment alone.

If we follow those steps and invest properly, then a good rule of thumb is this: in today’s dollars, you will need a minimum $1 million dollars to comfortably retire in Canada (and maybe even more depending on where).

To get to $1 million at retirement, assuming you make $50,000 per year, you should try to save at least 15% per year (if you start in your early 20s); if you start later, say in your 30s, try saving closer to 20%.

To get to $1 million at retirement, assuming you make $50,000 per year, you should try to save at least 15% per year (if you start in your early 20s); if you start later, say in your 30s, try saving closer to 20%.

For example: If a person is saving 15% of their income for the next 40 years and earns a 5% annual return on their investments (after fees), they’ll be able easily reach their goal. If that same person were only earning 2% instead of 5%, they would have to save as much as 22%.

Now let’s say that after 50 years of work and saving up an average of just over $1 million dollars (which is not unreasonable given how high house prices can be), we want our money invested so that it will grow over time while providing some income each month.

If you are entering your 40s with just a few thousand in savings, don’t worry too much – it’s better late than never! You can still save 15-20% of your paycheque each year and after 10 years, it will add up very nicely!

If you are entering your 40s with just a few thousand in savings, don’t worry too much – it’s better late than never! You can still save 15-20% of your paycheque each year and after 10 years, it will add up very nicely!

In fact, if you have been making steady contributions to your RRSP over the past 10 years (and have not withdrawn any money), then I would bet that you have more than enough assets to retire tomorrow. Let’s say that at age 45, your assets total $200k in stocks and bonds. Assuming an annual return of 5%, this would grow to $638k by age 55. If we assume that all these funds are invested conservatively (as opposed to taking on more risk) then at age 55 this portfolio could generate income of 8% per year ($52k). This means that even though our hypothetical investor has saved only $200k over the past decade (and did not take any withdrawals from their RRSPs), they could now retire comfortably at 55 without ever having contributed another cent!

Conclusion

After looking at the numbers and how much money you need for retirement, it is clear that if you want to retire comfortably, then you need to start planning early in life. A good rule of thumb is this: in today’s dollars, you will need a minimum $1 million dollars to comfortably retire in Canada. To get there at retirement age (average 65 years old), assuming your income doubles each year due to inflation, then it will take 10 years to save up enough money if you start saving 15% per year; if starting later than 30 years old then 20% per year would be necessary. If entering into your 40s with just a few thousand dollars saved up – don’t worry too much! You can still save 15-20% of your paycheque each year and after 10 years it adds up very nicely!