Avoid Debt

Exploring Canada’s Prime Interest Rate: A Key Indicator of Economic Stability

The prime interest rate is a crucial benchmark that significantly shapes Canada’s financial landscape. As a critical monetary policy tool, it influences borrowing costs, impacts the housing market, and reflects the overall state of the economy. In this article, we will delve into the prime interest rate in Canada, its importance, and how it affects various aspects of our daily lives.

Understanding the Prime Interest Rate: The prime interest rate represents the interest rate banks charge their most creditworthy customers for loans. It serves as the foundation for determining borrowing costs across various financial products, including mortgages, personal loans, business loans, and lines of credit. The Bank of Canada sets the target for the prime rate, which influences lending rates across the country.

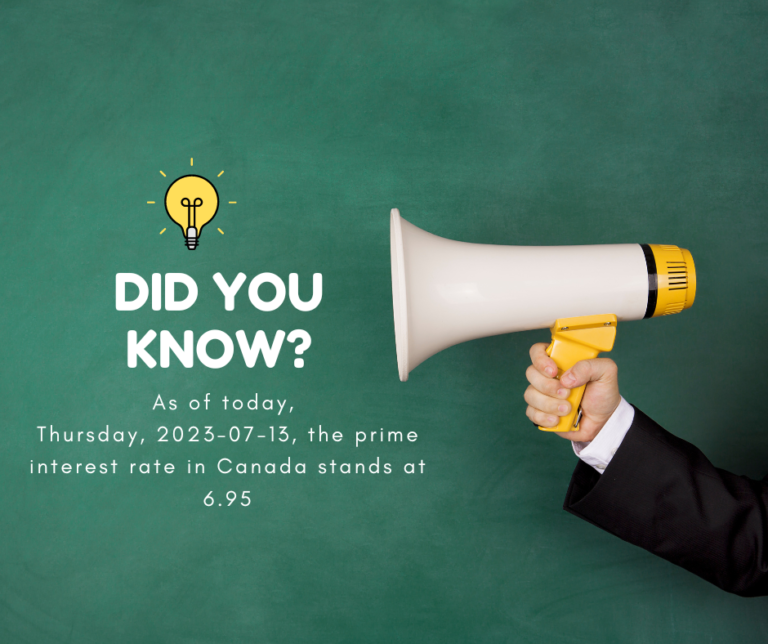

Current Prime Interest Rate in Canada: As of today, Thursday, 2023-07-13, the prime interest rate in Canada stands at 6.95%. It is important to note that the prime rate can fluctuate over time as economic conditions change. Financial institutions may adjust their prime rates accordingly, reflecting factors such as inflation, economic growth, and the monetary policy decisions of the central bank.

Impact on Borrowers: The prime interest rate directly affects borrowers in Canada. When the prime rate increases, borrowing costs rise, making it more expensive to take out loans or carry balances on lines of credit. Conversely, decreasing the prime rate can lead to lower borrowing costs, providing potential savings for borrowers. Homeowners with variable-rate mortgages are particularly impacted, as their interest rates can change when the prime rate fluctuates.

Influence on the Housing Market: The prime interest rate significantly influences the housing market. When the prime rate is high, mortgage rates tend to increase, making it more challenging for prospective homebuyers to afford homeownership. Conversely, a lower prime rate can stimulate the housing market by making mortgages more affordable and potentially increasing property demand. It is essential for individuals considering homeownership to monitor changes in the prime rate to make informed decisions.

Economic Indicator: The prime interest rate is also a crucial economic indicator. It reflects the central bank’s assessment of the country’s economic conditions and efforts to manage inflation and stimulate economic growth. When the prime rate is adjusted, it can signal the central bank’s stance on monetary policy and its views on the economy’s overall health.

The prime interest rate is a vital element of Canada’s financial system, influencing borrowing costs and reflecting the state of the economy. As of today, the prime rate in Canada stands at 6.95%. Understanding the prime rate’s impact on borrowing costs, the housing market, and its role as an economic indicator helps individuals make informed financial decisions. Keeping a close eye on changes in the prime rate can help borrowers and potential homeowners navigate the ever-changing financial landscape.

Debt Doldrums in Canada and How Canadian Customer Debt Relief can help

Debt Doldrums in Canada and How Canadian Customer Debt Relief can help

Canada is currently facing a significant challenge when it comes to consumer debt. Many Canadians find themselves caught in a cycle of debt, struggling to make ends meet and overcome their financial burdens. This article aims to shed light on the state of debt in Canada and highlight how Canadian Customer Debt Relief can provide much-needed assistance to those in need.

The State of Debt in Canada

In recent years, consumer debt levels in Canada have been steadily rising. According to the Bank of Canada, household debt reached a record high in 2022, surpassing $2.4 trillion. This staggering figure indicates that many Canadians live beyond their means and rely heavily on credit to finance their lifestyles.

Several factors contribute to the increasing debt burden faced by Canadians. One of the main culprits is the easy availability of credit, with credit cards and lines of credit readily accessible to consumers. Low-interest rates and enticing promotional offers often lure individuals into taking on more debt than they can handle.

The Impact of Debt on Canadian Consumers

The burden of debt has far-reaching consequences for Canadian consumers. Financial stress from overwhelming debt can affect individuals’ mental health and well-being. The constant worry about making monthly payments and the fear of falling behind can lead to anxiety, depression, and sleep disturbances.

Moreover, excessive debt limits consumers’ purchasing power and financial flexibility. High monthly debt payments eat into disposable income, leaving individuals with less money for essential expenses, savings, and investments. This can hinder their ability to achieve important life goals, such as homeownership or funding their children’s education.

Canadian Customer Debt Relief: How It Works

Canadian Customer Debt Relief is a reputable debt relief program designed to assist Canadians in overcoming their debt challenges. The program follows a structured process to provide effective and personalized debt relief solutions.

The first step in Canadian Customer Debt Relief is thoroughly assessing the individual’s financial situation. This involves evaluating their income, expenses, assets, and liabilities to understand their overall financial health comprehensively.

Based on this assessment, Canadian Customer Debt Relief develops a customized debt relief plan tailored to the individual’s needs and goals. This plan may involve a combination of debt-help strategies.

Canadian Customer Debt Relief provides ongoing support and guidance throughout the debt relief journey. Their team of financial experts offers advice on budgeting, money management, and improving credit scores. They aim to empower individuals with the necessary tools and knowledge to regain control of their finances and maintain a debt-free future.

Benefits of Canadian Customer Debt Relief

Engaging in a Canadian Customer Debt Relief program offers several benefits for individuals struggling with debt. Some of the key advantages include:

- Lower interest rates: Canadian Customer Debt Relief can secure 0% interest rates, reducing the overall cost of debt repayment.

- Reduced monthly payments: Through our debt help program, individuals can lower their monthly payments, making them more affordable and manageable within their budget.

- Consolidated debt management: Combining multiple debts into a single debt simplifies repayment. Instead of juggling various due dates and payment amounts, individuals only need to focus on a single monthly payment.

- Improved credit score: Completing a Canadian Customer Debt Relief program can improve an individual’s credit score. By consistently making timely payments and reducing debt, individuals demonstrate responsible financial behavior to credit agencies.

Conclusion

The escalating debt levels in Canada have put many individuals in challenging financial situations. However, Canadian Customer Debt Relief offers hope for those struggling with overwhelming debt. By providing personalized debt relief solutions, Canadian Customer Debt Relief aims to alleviate financial burdens and help individuals regain control of their finances.

Canadian Customer Debt Relief can tailor a customized plan that addresses their needs by assessing the individual’s financial situation. This personalized approach ensures that the debt relief strategy aligns with the individual’s goals and financial capabilities.

One of the primary advantages of Canadian Customer Debt Relief is 0% interest rates. The program secures a 0% interest rate, minimizing the overall cost of debt repayment. This can significantly ease the financial strain on individuals and expedite the path to debt freedom.

Additionally, Canadian Customer Debt Relief aims to reduce monthly payments, making them more manageable within the individual’s budget. By consolidating multiple debts into a single manageable payment, individuals can experience immediate relief and regain control over their financial obligations.

Consolidating debts into a single payment simplifies repayment and helps individuals stay organized and on top of their financial commitments. Instead of dealing with multiple due dates and varying payment amounts, individuals can focus on a single monthly payment, streamlining their debt management.

Another notable benefit of engaging in Canadian Customer Debt Relief is the potential for improving one’s credit score. By completing the debt relief program and consistently making timely payments, individuals can demonstrate responsible financial behavior to credit agencies. Over time, this can lead to an improved credit score, opening doors to better economic opportunities in the future.

In conclusion, the debt doldrums in Canada have created significant financial challenges for many individuals. However, Canadian Customer Debt Relief offers a beacon of hope, providing tailored debt relief solutions to help Canadians overcome their debt burdens.

FAQs

1. How long does completing a Canadian Customer Debt Relief program take? The duration of a Canadian Customer Debt Relief program varies depending on the individual’s financial situation and the selected debt relief strategies. It can take several months to a few years to complete the program successfully.

2. Will participating in a debt relief program affect my credit score? Engaging in a debt relief program may initially slightly impact your credit score. However, as you consistently make payments and reduce your debt through the program, your credit score has the potential to improve over time.

3. Can I still use credit cards while enrolled in a Canadian Customer Debt Relief program? Refraining from using credit cards while enrolled in a debt relief program is generally advisable. Limiting new credit usage allows you to repay your debts and improve your financial situation.

4. Will I be debt-free after completing a Canadian Customer Debt Relief program? Completing The Canadian Customer Debt Relief program will provide a pathway to becoming debt-free. However, it is essential to maintain responsible financial habits and avoid accumulating new debt after the program’s completion.

5. How do I get started with Canadian Customer Debt Relief? To get started with Canadian Customer Debt Relief, visit their website and provide the necessary information for a consultation. Their team will assess your financial situation and guide you through finding the most suitable debt relief solution for your needs.

In conclusion, Canadian Customer Debt Relief offers a comprehensive approach to tackling debt in Canada. Individuals can find relief from financial burdens by accessing personalized debt relief solutions and working towards a debt-free future. Remember, there is hope for a brighter financial future, and Canadian Customer Debt Relief is here to assist you on your journey to financial freedom.

10 Proven Ways to Get Out of Debt Faster in Canada

-

Table of Contents

- Introduction

- How to Create a Debt Repayment Plan to Get Out of Debt Faster in Canada

- How to Use Credit Cards to Your Advantage to Get Out of Debt Faster in Canada

- How to Negotiate with Creditors to Get Out of Debt Faster in Canada

- How to Take Advantage of Government Programs to Get Out of Debt Faster in Canada

- How to Utilize Debt Consolidation to Get Out of Debt Faster in Canada

- Conclusion

“Start Your Debt-Free Journey Today with 10 Proven Ways to Get Out of Debt Faster in Canada!”

Introduction

Are you struggling with debt in Canada? If so, you’re not alone. According to a recent survey, nearly half of Canadians are in debt, with the average household owing $1.77 for every dollar of disposable income. Fortunately, there are ways to get out of debt faster. In this article, we’ll discuss 10 proven ways to get out of debt faster in Canada. From budgeting and debt consolidation to debt settlement and credit counseling, we’ll cover all the options available to help you get out of debt faster. So, let’s get started!

How to Create a Debt Repayment Plan to Get Out of Debt Faster in Canada

Are you looking for a way to get out of debt faster in Canada? If so, creating a debt repayment plan is a great way to get started. A debt repayment plan is a strategy that helps you pay off your debt in a timely and organized manner. It can help you stay on track and make sure you don’t miss any payments. Here’s how to create a debt repayment plan to get out of debt faster in Canada.

Step 1: Calculate Your Total Debt

The first step in creating a debt repayment plan is to calculate your total debt. This includes all of your outstanding loans, credit cards, and other debts. Make sure to include the interest rate and minimum payment for each debt. This will give you an accurate picture of your total debt and help you create a realistic repayment plan.

Step 2: Prioritize Your Debts

Once you’ve calculated your total debt, it’s time to prioritize your debts. Start by focusing on the debts with the highest interest rates first. This will help you save money in the long run by reducing the amount of interest you pay. You should also prioritize any debts that have late fees or other penalties.

Step 3: Create a Budget

Creating a budget is an important part of any debt repayment plan. Start by listing your income and expenses. This will help you determine how much money you have available to put towards your debt each month. Make sure to include all of your fixed expenses, such as rent and utilities, as well as any variable expenses, such as groceries and entertainment.

Step 4: Make a Plan

Once you’ve created a budget, it’s time to make a plan. Start by setting a goal for how much you want to pay off each month. Then, divide that amount between your debts. Make sure to pay the minimum payment on each debt, plus any extra you can afford. This will help you pay off your debts faster and save money on interest.

Step 5: Track Your Progress

Finally, make sure to track your progress. This will help you stay motivated and on track with your debt repayment plan. You can use a spreadsheet or an app to track your payments and progress. This will also help you identify any areas where you can make adjustments to your budget or repayment plan.

Creating a debt repayment plan is a great way to get out of debt faster in Canada. By following these steps, you can create a plan that works for you and helps you pay off your debt in a timely and organized manner. Good luck!

How to Use Credit Cards to Your Advantage to Get Out of Debt Faster in Canada

Are you looking for ways to get out of debt faster in Canada? Credit cards can be a great tool to help you pay off your debt faster. Here are some tips to help you use credit cards to your advantage and get out of debt faster.

1. Pay more than the minimum balance. When you make a payment on your credit card, make sure to pay more than the minimum balance. This will help you pay off your debt faster and save you money in the long run.

2. Take advantage of balance transfer offers. Many credit cards offer balance transfer offers, which allow you to transfer your balance from one card to another with a lower interest rate. This can help you save money on interest and pay off your debt faster.

3. Use rewards programs. Many credit cards offer rewards programs that allow you to earn points or cash back on your purchases. These rewards can be used to pay off your debt faster or to purchase items you need.

4. Pay off your highest interest rate debt first. When you have multiple credit cards, it’s important to pay off the one with the highest interest rate first. This will help you save money on interest and pay off your debt faster.

5. Monitor your spending. It’s important to keep track of your spending and make sure you’re not overspending. This will help you stay on top of your debt and pay it off faster.

By following these tips, you can use credit cards to your advantage and get out of debt faster in Canada. With a little bit of planning and discipline, you can be debt-free in no time.

How to Negotiate with Creditors to Get Out of Debt Faster in Canada

Are you looking for ways to get out of debt faster in Canada? Negotiating with creditors can be a great way to reduce your debt and get back on track financially. Here are some tips to help you negotiate with creditors and get out of debt faster.

1. Know Your Rights: Before you start negotiating with creditors, it’s important to understand your rights. In Canada, you have the right to negotiate with creditors to reduce your debt. You also have the right to dispute any inaccurate information on your credit report.

2. Be Prepared: Before you start negotiating with creditors, make sure you have all the information you need. This includes your current financial situation, a list of your debts, and a budget. Knowing your financial situation will help you make informed decisions when negotiating with creditors.

3. Be Honest: When negotiating with creditors, it’s important, to be honest about your financial situation. Don’t try to hide any information or make false promises. Creditors are more likely to work with you if they know you’re being honest.

4. Make an Offer: Once you’ve gathered all the information you need, it’s time to make an offer. Make sure your offer is reasonable and that you can afford to make the payments. If the creditor agrees to your offer, make sure you get it in writing.

5. Follow Through: Once you’ve reached an agreement with the creditor, it’s important to follow through. Make sure you make all the payments on time and keep track of your progress. This will help you stay on track and get out of debt faster.

Negotiating with creditors can be a great way to reduce your debt and get out of debt faster in Canada. By following these tips, you can make sure you’re prepared and get the best deal possible. Good luck!

How to Take Advantage of Government Programs to Get Out of Debt Faster in Canada

Are you struggling with debt in Canada? You’re not alone. Many Canadians are in the same boat. But the good news is that there are government programs available to help you get out of debt faster. Here’s how to take advantage of them.

1. Take advantage of the Bankruptcy and Insolvency Act. This act allows you to file for bankruptcy if you’re unable to pay your debts. It can help you get out of debt faster by allowing you to have your debts discharged or restructured.

2. Take advantage of the Consumer Proposal Program. This program allows you to make a proposal to your creditors to pay back a portion of your debt. This can help you get out of debt faster by reducing the amount you owe.

3. Take advantage of the Credit Counselling Services of Canada. This organization provides free credit counseling services to help you manage your debt. They can help you create a budget, negotiate with creditors, and develop a plan to get out of debt faster.

4. Take advantage of the Canada Student Loans Program. This program provides financial assistance to students who are struggling with debt. It can help you get out of debt faster by providing you with the funds you need to pay off your loans.

5. Take advantage of the Canada Pension Plan. This program provides financial assistance to seniors who are struggling with debt. It can help you get out of debt faster by providing you with the funds you need to pay off your debts.

By taking advantage of these government programs, you can get out of debt faster and start living a debt-free life. So don’t wait any longer – take action today and start taking advantage of these programs!

How to Utilize Debt Consolidation to Get Out of Debt Faster in Canada

Are you struggling with debt in Canada? If so, you’re not alone. Many Canadians are in the same boat, and it can be difficult to know where to turn for help. One option that can help you get out of debt faster is debt consolidation.

Debt consolidation is a process that involves taking out a loan to pay off multiple debts. This can help you simplify your finances and make it easier to manage your debt. It can also help you save money on interest and fees.

When you consolidate your debt, you’ll take out a loan to pay off all of your existing debts. This loan will usually have a lower interest rate than your existing debts, so you’ll save money on interest and fees. You’ll also have just one payment to make each month, which can make it easier to manage your finances.

There are a few different types of debt consolidation loans available in Canada. You can take out a personal loan, a home equity loan, or a line of credit. Each option has its own advantages and disadvantages, so it’s important to do your research and find the best option for your situation.

When you’re considering debt consolidation, it’s important to make sure you’re making the right decision. Make sure you understand the terms of the loan and the repayment schedule. You should also make sure you’re not taking on more debt than you can handle.

Debt consolidation can be a great way to get out of debt faster in Canada. It can help you save money on interest and fees, and make it easier to manage your finances. Just make sure you do your research and make sure it’s the right decision for your situation.

Conclusion

In conclusion, 10 Proven Ways to Get Out of Debt Faster in Canada is a great resource for anyone looking to get out of debt quickly and efficiently. By following the tips outlined in this article, Canadians can make a plan to pay off their debt faster and get back on track financially. With the right strategies and dedication, Canadians can become debt-free and enjoy the financial freedom they deserve.

The Divide between Must-Haves and Nice-to-Haves: How Canadian Customer Debt Relief Can Help

In today’s world of endless options and endless possibilities, it can be challenging to determine what is truly essential and what is simply a want. The line between needs and wants is often blurred, making it difficult to prioritize and make sound financial decisions. This is where Canadian Customer Debt Relief can help, by providing guidance and support in distinguishing between the two.

A need is something that is essential for survival or well-being. These are the things we cannot live without, such as food, shelter, clothing, and medical care. These necessities are required for our physical and emotional well-being, and without them, we cannot lead a healthy and fulfilling life.

Wants, on the other hand, are things we desire but do not need to survive. These are items or experiences that bring us pleasure, such as a new car, a vacation, or a designer handbag. Wants are not essential to our survival, but they can improve our quality of life.

Canadian Customer Debt Relief can assist in identifying the difference between needs and wants by providing tools and resources to help prioritize spending and make more informed financial decisions. By understanding what is essential and allocating resources accordingly, individuals can avoid overspending on items that bring temporary pleasure but do not add long-term value to their lives.

To determine whether an item is a need or a want, Canadian Customer Debt Relief suggests asking yourself the following questions:

- Will my life be affected if I don’t have this item?

- Is this item necessary for my physical or emotional well-being?

- Can I live without this item and still be happy?

By answering these questions, individuals can gain a better understanding of what is truly important and what is simply a desire. Canadian Customer Debt Relief can provide additional support and resources to help make informed financial decisions, including debt management plans, budgeting tools, and credit counseling services.

The divide between needs and wants is crucial in making informed financial decisions. Understanding the difference between what is essential and what is simply a desire allows individuals to prioritize their spending and allocate their resources accordingly. With the support of Canadian Customer Debt Relief, individuals can lead a more balanced and fulfilling life, free from the burden of debt and financial stress.

Why it is Important to Avoid Debt

Debt is a necessary part of life. You need to borrow money in order to buy a house, start a business or go on vacation. However, it’s important that you avoid debt whenever possible. There are many reasons why you should avoid becoming too dependent on debt and some of them include:

Debt does not go away by itself

Debt is a long-term problem, and it won’t just go away.

It’s important to understand that debt doesn’t disappear on its own. There are many people who think they can just ignore their debt and it will eventually go away, but this isn’t true at all! The only way for your debt to truly disappear is if you take action. If you don’t take action, then your situation will continue to get worse until you start having problems with your finances and other areas of life as well.

Debt affects more than just your finances; it also affects your emotions.

Remember: Debt isn’t just a financial problem; it also has emotional consequences as well. As far as mental health goes, dealing with debt can be very stressful and exhausting—and sometimes even downright depressing! However if one approaches their situation with positivity instead of negativity (i.e., says something like “I’m going through a tough time right now but I know things will turn around soon”) then they’ll end up feeling much better about themselves by staying positive despite all odds stacked against them today or tomorrow…or whenever else they might encounter problems caused by someone else’s mistake (in this case being responsible enough not only pay off all debts owed but also never get into any kind of trouble again).

Debt can lead to bankruptcy and foreclosure.

While it may sound extreme, bankruptcy and foreclosure are a reality for many Canadians. Bankruptcy is a legal process that allows you to deal with debt, while foreclosure is the legal process of dealing with debt by selling your house to pay off any outstanding loans.

Regardless of the type of debt you have, both processes can be avoided if you are proactive in taking care of things before they get out of hand.

Debt carries hidden fees that you may not be aware of.

Hidden fees are charges that you didn’t know about at the time of signing. Hidden fees can be charged by lenders or credit card companies and can include interest rates, transaction fees, annual fees and late payment penalties. If you are not aware of these fees it may be difficult to budget for them or plan ways to avoid paying them in the future.

In addition to being a financial burden, debt can negatively affect your emotional well-being.

In addition to being a financial burden, debt can negatively affect your emotional well-being.

You may not realize that your finances are making you anxious, depressed or even suicidal until it’s too late. Be aware of the following signs:

- You feel like you’re drowning in debt. If this is how you feel, it may be time to seek help from someone who can assist you with gaining control over your finances once again.

- Your relationships are suffering because of money issues. For example, if you are unable to pay for necessities such as rent and utilities without asking friends or family members for help, it could lead them to resent having to take care of an adult who is “wasting money on frivolous things.”

Problems with debt can cause severe financial problems.

In addition to the obvious costs incurred from paying interest on a debt, there is a host of other problems that can arise from taking on debt. For example, having too much debt can affect your credit score and ability to get a loan. If you have too many loans or high balances on your accounts, it can make it difficult for lenders to determine whether or not they should trust you with a new loan or credit card. Even worse, if you have no money in savings and few assets besides whatever assets are already secured by mortgages or car loans (like a house or car), then there may be nothing available for lenders to take if they need to foreclose on their collateralized property.

In addition to potentially hurting your ability to purchase property or buy things like cars in the future (due to negative equity), taking out too much debt could also prevent people from buying those important things now due simply because they don’t have enough income left over after paying bills each month! This means that even though someone might really want something nice like an iPhone X but know full well that making payments every month will mean less money left over at month’s end so only having enough money after all bills are paid each month – then maybe buying one isn’t worth doing at this point because then where does one find funds for food/rent/etcetera?”

Avoiding debt is so important because it causes emotional pain and financial hardship.

So, why is it important to avoid debt? The answer is simple: debt can cause emotional pain and financial hardship.

When you are in a lot of debt, or when you have a high credit card balance, it can be stressful. You might become anxious about not being able to make ends meet each month and worry about where the money for your bills is going to come from.

This stress can lead to depression if it continues for too long. It’s also common for people who are struggling financially due to their debt problems not only feel stressed but also anxious and depressed as well as angry with themselves or others around them who caused them these problems like their spouse or close friends/family members who aren’t helping understand what they feel like when they see each other at work because they know how much money we owe every month which makes things worse because there’s nothing anyone else could do right now except let me know that everything’s going ok?”

Conclusion

We hope this article has helped you understand why it is important not to get into debt. If you are suffering from debt, we would like to encourage you to seek help from a financial advisor or credit counselor. They will be able to help you with your situation and make sure that your future finances stay on track!