Signs That You Need Debt Help

We’ve all faced tough financial times, but how do you know when your debt has become unmanageable? While borrowing money isn’t inherently wrong, there are warning signs that your debt may spiral out of control. Let’s take a deep dive into these signs.

Struggling to Meet Minimum Payments

The early stages of debt trouble often begin with missing the occasional payment.

Why it’s a concern

If you’re consistently struggling to make even the minimum payments on your bills, it’s a glaring sign that your finances need a severe overhaul. After all, these payments are designed to be achievable.

Real-life scenarios

Imagine Jane, who once quickly paid off her monthly credit card balance. But now, with rising expenses and stagnant income, she can only pay the minimum, accruing interest at a rate she didn’t anticipate.

Taking on New Debt to Pay Off Old Debt

This is a classic sign of being trapped in a vicious debt cycle.

The debt cycle

Think of it as using one credit card to pay off another. It’s like digging a hole to fill another – you’re only moving the problem, not solving it.

Long-term effects

The interest accumulates, and before you realize it, you owe much more than you borrowed in the first place.

Avoiding Calls from Creditors

If you cringe whenever the phone rings, fearing it’s a creditor, there’s cause for concern.

Consequences of ignoring

Avoidance can lead to severe consequences, like increased interest rates, additional fees, and legal actions.

Personal stories

Consider Tom, who chose to ignore creditor calls. It impacted his credit score and added stress to his daily life.

Sleepless Nights over Money Worries

Money troubles don’t just affect your bank account—they can also wreak havoc on your well-being.

Mental health implications

The debt stress can lead to anxiety, depression, and sleepless nights. When left unchecked, these concerns can spiral, affecting other areas of your life.

Health tips and guidance

If money worries are causing sleepless nights, consider speaking to a therapist. Financial stress is natural, and there’s no shame in seeking help.

Conclusion

Debt issues, if unchecked, can spiral out of control. But recognizing the signs early can be a lifesaver. Whether making a budget, consolidating debt, or seeking professional advice, the first step to resolution is recognizing the problem. Remember, it’s okay to seek help. You’re not alone in this.

FAQs

- What are the first signs of debt problems?

- Struggling with minimum payments and avoiding creditor calls are often early indicators.

- Can ignoring creditor calls lead to legal consequences?

- Yes, it can lead to increased rates, added fees, and even legal actions.

- How does debt affect mental health?

- Financial stress can lead to anxiety, depression, and sleep disturbances.

- Where can I get debt help?

- Seek financial advisors, credit counseling agencies, self-help books, and online resources.

- Is it wrong to use one loan to pay off another?

- It’s generally a sign of a worsening debt situation, which can lead to more debt in the long run.

CCDR: Canada’s #1 Canadian Debt Relief Program

Introduction to CCDR

Hey there, fellow Canadian! Are you drowning in debt and feeling overwhelmed? What if I told you there’s a lifebuoy designed just for you? Enter CCDR – the top-notch Canadian Debt Relief Program.

What is CCDR?

The Canadian Customer Debt Relief (CCDR) program is a tailored solution designed for Canadians like you, navigating the challenging waters of debt. It’s more than just a service; it’s a commitment to bring you back to financial stability.

Why CCDR Stands Out

Debt relief options are plenty, but CCDR has earned its reputation as Canada’s #1 choice. Why? Because they understand the unique financial intricacies Canadians face and offer solutions that are both effective and empathetic.

The Need For Debt Relief In Canada

Ever felt like you’re on a treadmill of debt? You’re not alone.

The Canadian Debt Scenario

Recent stats indicate an alarming rise in Canadian household debt. From mortgages to credit card bills, we’re juggling more financial balls than ever before. And sometimes, a few of those balls drop.

How Debt Can Impact Your Life

Ever missed a friend’s wedding because you couldn’t afford it? Or been sleep-deprived, stressing about bills? The chains of debt aren’t just financial. They tug at our mental well-being and quality of life.

How CCDR Works

Let’s demystify the process.

The Process

- Assessment: Begin with a comprehensive review of your financial situation.

- Customized Plan: Craft a debt-relief plan that suits your needs and goals

- Execution: With experts by your side, embark on your journey to debt freedom.

Benefits of Using CCDR

- Expert Guidance: CCDR professionals have extensive experience and knowledge.

- Tailored Solutions: One size doesn’t fit all. CCDR knows that.

- Peace of Mind: Sleep better, knowing your financial future is in safe hands.

CCDR’s proven track record and tailor-made solutions set them apart.

Visit CCDR’s official website and start with a free assessment!

Absolutely! Their testimonials and success rates speak volumes.

It varies based on individual debt, but CCDR aims to expedite relief as swiftly as possible.

Transparency is a cornerstone of CCDR—no hidden fees. No surprises.

Steps to Start Your Debt-Free Journey

Remember, the journey of a thousand miles begins with a single step. So, why wait? Initiate your debt-relief journey with CCDR now!

Life’s too short to be spent worrying about debts. And with CCDR, you don’t have to. Opt for Canada’s #1 debt relief program and embark on a journey to financial freedom. Ready to break free from the shackles of debt? Let CCDR be your guiding light.

How Debt Impacts the Mental Health of Canadians: A Comprehensive Guide

In the hustle and bustle of modern life, financial matters often take center stage. For Canadians, managing debt has become an integral part of the daily routine. However, what’s often overlooked is the significant impact that debt can have on mental health. This article delves into the intricate connection between financial debt and the mental well-being of Canadians. We’ll explore how debt influences emotional and psychological states and provide practical strategies for managing the resulting challenges.

How Debt Impacts the Mental Health of Canadians

Debt isn’t just a financial burden; it can also cast a long shadow on mental health. The growing concerns have prompted researchers and psychologists to investigate the link between financial struggles and emotional well-being.

The Anxiety Avalanche

Debt often acts as a catalyst for anxiety, triggering a snowball effect on mental health. The constant worry about repayment deadlines, interest rates, and collection calls can lead to sleepless nights and heightened stress levels. As individuals grapple with the weight of debt, their overall quality of life can deteriorate.

The Isolation Paradox

Mounting debt can foster feelings of shame and embarrassment, causing individuals to withdraw from social circles. The fear of judgment and the desire to maintain appearances may drive people to isolate themselves, intensifying their emotional struggles.

Navigating the Depression Quagmire

Prolonged financial stress due to debt can deepen feelings of hopelessness and depression. Feelings of inadequacy and an inability to provide for oneself or loved ones can take a heavy toll on mental health.

The Self-Worth Conundrum

Debt can erode one’s sense of self-worth, as individuals tie their financial situation to their value as individuals. This self-imposed judgment can lead to a downward spiral of negative thoughts and emotions.

Cognitive Load Overload

Debt-related stress can overwhelm cognitive functions, impairing decision-making abilities. When the mind is preoccupied with financial worries, it leaves less room for productive thoughts and problem-solving skills.

Strained Relationships: Love and Money

Debt can put immense strain on personal relationships. Conflicts about money can escalate, leading to breakdowns in communication and trust within families and partnerships.

Strategies for Managing Debt-Related Mental Health Challenges

- Seek Professional Guidance – If debt is taking a toll on your mental health, consider consulting a financial advisor or a mental health professional. They can provide tailored advice to alleviate both your financial and emotional burden.

- Open Dialogue and Communication – Breaking the silence around debt can be liberating. Engage in open conversations with loved ones about your financial struggles. Supportive relationships can offer comfort and alleviate feelings of isolation.

- Mindfulness and Stress Reduction – Incorporating mindfulness practices into your routine can help manage stress. Meditation and deep breathing can promote relaxation and provide mental clarity amidst financial challenges.

- Set Realistic Goals – Instead of focusing solely on clearing debt, set realistic goals considering your financial situation. Celebrate small victories, and remember that progress takes time.

- Budgeting and Financial Planning – Creating and sticking to a budget can provide a sense of control over your finances. Allocate funds for debt repayment while ensuring you have resources for daily needs and leisure activities.

- Prioritize Self-Care – Amidst debt-related stress, prioritize self-care. Engage in activities that bring joy, practice self-compassion, and remember that your financial situation doesn’t solely define your worth.

FAQs about Debt and Mental Health

While debt may not directly cause clinical depression, it can contribute to feelings of hopelessness and exacerbate existing mental health conditions.

Seeking professional guidance can provide valuable insights and strategies to manage debt-related stress’s financial and emotional aspects.

Open communication is critical. Discuss your financial concerns with your partner, establish joint financial goals, and work together to find solutions.

Yes, mindfulness techniques can promote relaxation and reduce stress. Focusing on the present moment can alleviate the overwhelming nature of debt-related worries.

Focus on your strengths and achievements outside of your financial situation. Engage in activities you’re passionate about and seek validation from sources beyond money.

Absolutely. Maintaining a positive outlook involves reframing your perspective, setting achievable goals, and prioritizing self-care and personal growth.

The connection between debt and mental health for Canadians is undeniable. The emotional toll of financial struggles can be significant, impacting various aspects of life. However, with proactive steps, open communication, and self-care, individuals can effectively manage the challenges posed by debt-related stress. Remember, seeking support from professionals, friends, and family can make a world of difference in navigating this intricate relationship between financial well-being and mental health.

Back to School Budgeting: Smart Strategies for a Smooth Start

Are you ready for the upcoming school year? As the back-to-school season approaches, it’s essential to prepare your child and your budget. Balancing the costs of supplies, clothing, and other necessities can be daunting, but with the right strategies, you can ensure a smooth and stress-free transition. In this article, we’ll explore practical ways to budget for the back-to-school season while keeping your finances in check.

Creating a Comprehensive Back-to-School Budget

- Assess Your Needs and Prioritize Before embarking on your back-to-school shopping journey, take some time to assess your needs. List essential items such as school supplies, uniforms, backpacks, and electronics. Prioritize these items based on their urgency and importance. This step will help you allocate your budget more effectively.

- Set a Realistic Spending Limit. Determine how much you can comfortably spend on back-to-school expenses without straining your finances. Consider your overall financial situation, including income and other financial commitments. Setting a spending limit will prevent overspending and ensure you stay within your means.

- Research and Compare Prices Take advantage of online resources and local store flyers to research and compare prices for different items. Look for sales, discounts, and special offers that can help you save money. Remember, a little extra effort in comparing prices can lead to significant savings in the long run.

- Involve Your Children Include your children in the budgeting process. Discuss the budget constraints with them and encourage them to make thoughtful decisions when selecting items. This teaches them about financial responsibility and helps them understand the value of money.

Smart Shopping Strategies

- Shop Early and Spread Out Purchases Avoid the last-minute rush by starting your shopping early. You can use different sales and deals by spreading your purchases over a few weeks. This approach also allows you to avoid impulse buying, which can lead to unnecessary expenses.

- Buy Secondhand When Possible Consider purchasing secondhand items such as textbooks, clothing, and electronics. Online platforms and thrift stores often have gently used items at a fraction of the cost. Just be sure to inspect the items for quality before making a purchase.

- Utilize Coupons and Cashback Offers. Clip coupons from newspapers or digital coupon apps to save on various items. Additionally, consider using cashback websites or credit cards that offer cashback rewards on back-to-school purchases. Every little bit of savings adds up!

Transitioning Back to School Smoothly

- Prepare Meals at Home Packing lunches and snacks at home can help you save a significant amount of money compared to buying from school cafeterias or fast-food establishments. Plan nutritious and budget-friendly meals that your child will enjoy.

- Explore Free or Low-Cost Activities Instead of spending money on costly after-school programs or entertainment, explore free or low-cost activities in your community. Libraries, parks, and community centers often offer educational and recreational options for children.

- Encourage Open Communication Keep the lines of communication open with your child about budgeting and spending. Discuss the importance of making responsible choices and the value of money. By fostering these conversations, you empower your child to develop strong financial habits from a young age.

Navigating the back-to-school season with a well-structured budget is a prudent approach that benefits your finances and your child’s education. You can make the most of this exciting time by assessing your needs, setting limits, and employing savvy shopping strategies without breaking the bank. Remember, careful planning and thoughtful spending will ensure a successful transition back to school while keeping your financial goals intact.

Getting Rid of Debt Before Retirement in Canada

Retirement is a phase of life most Canadians look forward to, dreaming of days without deadlines, meetings, or work stress. But what if the looming specter of debt clouds your hard-earned retirement? Well, worry not. This article will guide you through achieving a debt-free retirement in Canada.

The Necessity of a Debt-Free Retirement

Entering your golden years with a pile of debt can be a massive strain on your retirement savings. You’ve worked diligently to enjoy this period, so why let debt ruin it? Moreover, without a regular income, managing debt can be a daunting task. Thus, it’s crucial to get rid of your debt before retiring.

Understanding the Types of Debt

Before planning your debt elimination, it’s essential to understand the different types of debt that you might be dealing with.

Credit Card Debt

This is one of the most common forms of debt. High-interest rates can make it a significant burden if not promptly addressed.

Mortgage Debt

While having your house paid off by retirement is ideal, it isn’t always possible. Still, reducing this debt can significantly decrease your financial stress.

Auto Loans

If you’re still paying off your car, consider if it’s necessary. It might be worth considering if public transportation or a cheaper vehicle can serve your needs.

The Impact of Debt on Retirement

Carrying debt into retirement isn’t just about numbers. It can have far-reaching implications.

Financial Implications

Debt can drain your retirement savings, limiting your ability to enjoy the retirement lifestyle you’ve dreamed of.

Psychological Implications

The stress from debt can impact your mental health, diminishing your overall quality of life during retirement.

Strategies to Overcome Debt

The road to a debt-free retirement may seem challenging, but various strategies can help you overcome your debt.

Debt Consolidation

This involves combining all your debts into one, often with a lower interest rate, making it easier to manage and pay off.

Debt Settlement

With debt settlement, you negotiate with your creditors to allow you to pay a lump sum that’s less than what you owe.

Filing for Bankruptcy

While this should be your last resort, in extreme cases, filing for bankruptcy can help eliminate debt. Be sure to consult with a financial advisor before making this decision.

How CCDR Can Assist in Your Journey

At Canadian Customer Debt Relief Inc. (CCDR), we’re committed to helping Canadians like you overcome debt. With our A+ BBB rating and over two decades of experience, we’ve assisted countless individuals in navigating their path to a debt-free retirement.

Importance of Early Planning

The earlier you start, the easier it’ll be to handle your debt.

Setting Up a Budget

Creating and sticking to a budget can help you manage expenses and save more.

Increasing Your Income

Consider part-time jobs or freelancing to earn extra income that can be put towards paying off debt.

Investing Wisely

Investments can be a great source of passive income if done wisely.

Conclusion

Retirement should be a time of relaxation, not financial stress. Planning early and wisely can rid yourself of debt and pave the way for a peaceful retirement. CCDR is here to help you in this journey toward a debt-free retirement.

FAQs

1. What is the most common type of debt among retirees?

Credit card debt is often the most common, followed by mortgage debt.

2. Is it too late to plan a debt-free retirement in my 50s?

No, it’s never too late to start planning. However, earlier planning can give you more options and flexibility.

3. Can CCDR help with all types of debts?

Yes, CCDR assists with most types of unsecured debt.

4. What are the psychological impacts of debt in retirement?

Debt in retirement can lead to stress, anxiety, and even depression due to financial insecurity.

5. How can investing help in achieving a debt-free retirement?

Investing can provide a source of passive income that can be used to pay off debt.

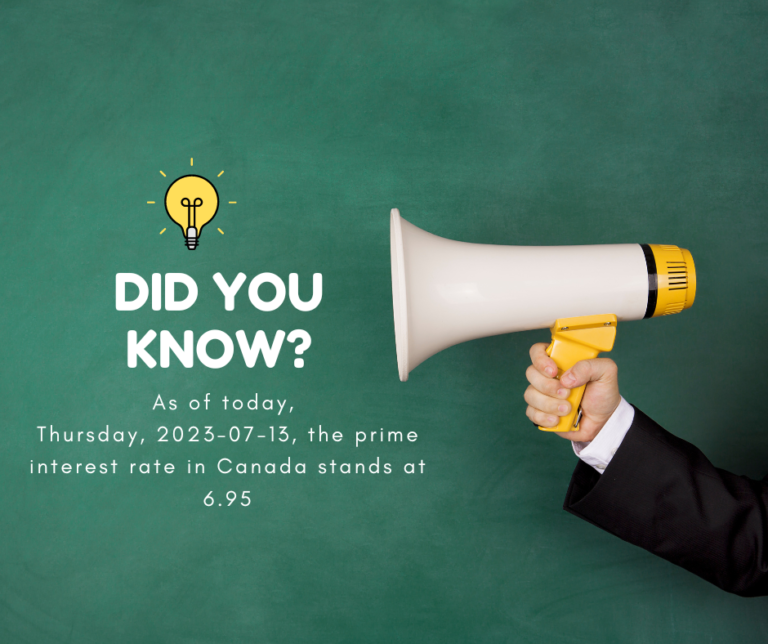

Exploring Canada’s Prime Interest Rate: A Key Indicator of Economic Stability

The prime interest rate is a crucial benchmark that significantly shapes Canada’s financial landscape. As a critical monetary policy tool, it influences borrowing costs, impacts the housing market, and reflects the overall state of the economy. In this article, we will delve into the prime interest rate in Canada, its importance, and how it affects various aspects of our daily lives.

Understanding the Prime Interest Rate: The prime interest rate represents the interest rate banks charge their most creditworthy customers for loans. It serves as the foundation for determining borrowing costs across various financial products, including mortgages, personal loans, business loans, and lines of credit. The Bank of Canada sets the target for the prime rate, which influences lending rates across the country.

Current Prime Interest Rate in Canada: As of today, Thursday, 2023-07-13, the prime interest rate in Canada stands at 6.95%. It is important to note that the prime rate can fluctuate over time as economic conditions change. Financial institutions may adjust their prime rates accordingly, reflecting factors such as inflation, economic growth, and the monetary policy decisions of the central bank.

Impact on Borrowers: The prime interest rate directly affects borrowers in Canada. When the prime rate increases, borrowing costs rise, making it more expensive to take out loans or carry balances on lines of credit. Conversely, decreasing the prime rate can lead to lower borrowing costs, providing potential savings for borrowers. Homeowners with variable-rate mortgages are particularly impacted, as their interest rates can change when the prime rate fluctuates.

Influence on the Housing Market: The prime interest rate significantly influences the housing market. When the prime rate is high, mortgage rates tend to increase, making it more challenging for prospective homebuyers to afford homeownership. Conversely, a lower prime rate can stimulate the housing market by making mortgages more affordable and potentially increasing property demand. It is essential for individuals considering homeownership to monitor changes in the prime rate to make informed decisions.

Economic Indicator: The prime interest rate is also a crucial economic indicator. It reflects the central bank’s assessment of the country’s economic conditions and efforts to manage inflation and stimulate economic growth. When the prime rate is adjusted, it can signal the central bank’s stance on monetary policy and its views on the economy’s overall health.

The prime interest rate is a vital element of Canada’s financial system, influencing borrowing costs and reflecting the state of the economy. As of today, the prime rate in Canada stands at 6.95%. Understanding the prime rate’s impact on borrowing costs, the housing market, and its role as an economic indicator helps individuals make informed financial decisions. Keeping a close eye on changes in the prime rate can help borrowers and potential homeowners navigate the ever-changing financial landscape.

Debt Doldrums in Canada and How Canadian Customer Debt Relief can help

Debt Doldrums in Canada and How Canadian Customer Debt Relief can help

Canada is currently facing a significant challenge when it comes to consumer debt. Many Canadians find themselves caught in a cycle of debt, struggling to make ends meet and overcome their financial burdens. This article aims to shed light on the state of debt in Canada and highlight how Canadian Customer Debt Relief can provide much-needed assistance to those in need.

The State of Debt in Canada

In recent years, consumer debt levels in Canada have been steadily rising. According to the Bank of Canada, household debt reached a record high in 2022, surpassing $2.4 trillion. This staggering figure indicates that many Canadians live beyond their means and rely heavily on credit to finance their lifestyles.

Several factors contribute to the increasing debt burden faced by Canadians. One of the main culprits is the easy availability of credit, with credit cards and lines of credit readily accessible to consumers. Low-interest rates and enticing promotional offers often lure individuals into taking on more debt than they can handle.

The Impact of Debt on Canadian Consumers

The burden of debt has far-reaching consequences for Canadian consumers. Financial stress from overwhelming debt can affect individuals’ mental health and well-being. The constant worry about making monthly payments and the fear of falling behind can lead to anxiety, depression, and sleep disturbances.

Moreover, excessive debt limits consumers’ purchasing power and financial flexibility. High monthly debt payments eat into disposable income, leaving individuals with less money for essential expenses, savings, and investments. This can hinder their ability to achieve important life goals, such as homeownership or funding their children’s education.

Canadian Customer Debt Relief: How It Works

Canadian Customer Debt Relief is a reputable debt relief program designed to assist Canadians in overcoming their debt challenges. The program follows a structured process to provide effective and personalized debt relief solutions.

The first step in Canadian Customer Debt Relief is thoroughly assessing the individual’s financial situation. This involves evaluating their income, expenses, assets, and liabilities to understand their overall financial health comprehensively.

Based on this assessment, Canadian Customer Debt Relief develops a customized debt relief plan tailored to the individual’s needs and goals. This plan may involve a combination of debt-help strategies.

Canadian Customer Debt Relief provides ongoing support and guidance throughout the debt relief journey. Their team of financial experts offers advice on budgeting, money management, and improving credit scores. They aim to empower individuals with the necessary tools and knowledge to regain control of their finances and maintain a debt-free future.

Benefits of Canadian Customer Debt Relief

Engaging in a Canadian Customer Debt Relief program offers several benefits for individuals struggling with debt. Some of the key advantages include:

- Lower interest rates: Canadian Customer Debt Relief can secure 0% interest rates, reducing the overall cost of debt repayment.

- Reduced monthly payments: Through our debt help program, individuals can lower their monthly payments, making them more affordable and manageable within their budget.

- Consolidated debt management: Combining multiple debts into a single debt simplifies repayment. Instead of juggling various due dates and payment amounts, individuals only need to focus on a single monthly payment.

- Improved credit score: Completing a Canadian Customer Debt Relief program can improve an individual’s credit score. By consistently making timely payments and reducing debt, individuals demonstrate responsible financial behavior to credit agencies.

Conclusion

The escalating debt levels in Canada have put many individuals in challenging financial situations. However, Canadian Customer Debt Relief offers hope for those struggling with overwhelming debt. By providing personalized debt relief solutions, Canadian Customer Debt Relief aims to alleviate financial burdens and help individuals regain control of their finances.

Canadian Customer Debt Relief can tailor a customized plan that addresses their needs by assessing the individual’s financial situation. This personalized approach ensures that the debt relief strategy aligns with the individual’s goals and financial capabilities.

One of the primary advantages of Canadian Customer Debt Relief is 0% interest rates. The program secures a 0% interest rate, minimizing the overall cost of debt repayment. This can significantly ease the financial strain on individuals and expedite the path to debt freedom.

Additionally, Canadian Customer Debt Relief aims to reduce monthly payments, making them more manageable within the individual’s budget. By consolidating multiple debts into a single manageable payment, individuals can experience immediate relief and regain control over their financial obligations.

Consolidating debts into a single payment simplifies repayment and helps individuals stay organized and on top of their financial commitments. Instead of dealing with multiple due dates and varying payment amounts, individuals can focus on a single monthly payment, streamlining their debt management.

Another notable benefit of engaging in Canadian Customer Debt Relief is the potential for improving one’s credit score. By completing the debt relief program and consistently making timely payments, individuals can demonstrate responsible financial behavior to credit agencies. Over time, this can lead to an improved credit score, opening doors to better economic opportunities in the future.

In conclusion, the debt doldrums in Canada have created significant financial challenges for many individuals. However, Canadian Customer Debt Relief offers a beacon of hope, providing tailored debt relief solutions to help Canadians overcome their debt burdens.

FAQs

1. How long does completing a Canadian Customer Debt Relief program take? The duration of a Canadian Customer Debt Relief program varies depending on the individual’s financial situation and the selected debt relief strategies. It can take several months to a few years to complete the program successfully.

2. Will participating in a debt relief program affect my credit score? Engaging in a debt relief program may initially slightly impact your credit score. However, as you consistently make payments and reduce your debt through the program, your credit score has the potential to improve over time.

3. Can I still use credit cards while enrolled in a Canadian Customer Debt Relief program? Refraining from using credit cards while enrolled in a debt relief program is generally advisable. Limiting new credit usage allows you to repay your debts and improve your financial situation.

4. Will I be debt-free after completing a Canadian Customer Debt Relief program? Completing The Canadian Customer Debt Relief program will provide a pathway to becoming debt-free. However, it is essential to maintain responsible financial habits and avoid accumulating new debt after the program’s completion.

5. How do I get started with Canadian Customer Debt Relief? To get started with Canadian Customer Debt Relief, visit their website and provide the necessary information for a consultation. Their team will assess your financial situation and guide you through finding the most suitable debt relief solution for your needs.

In conclusion, Canadian Customer Debt Relief offers a comprehensive approach to tackling debt in Canada. Individuals can find relief from financial burdens by accessing personalized debt relief solutions and working towards a debt-free future. Remember, there is hope for a brighter financial future, and Canadian Customer Debt Relief is here to assist you on your journey to financial freedom.

10 Tips for Maintaining a Healthy Budget at Home

Maintaining a healthy budget at home has become more critical today, where everything seems to be getting expensive daily. As a result, we have to be more mindful of our finances and keep our expenses in check. This article will provide ten practical tips for maintaining a healthy budget at home.

Create a budget plan

Creating a budget plan is the first step in maintaining a healthy home budget. This will help you keep track of your expenses and identify areas where you can cut down your costs. Next, list your monthly income and expenses, including your bills, groceries, and other miscellaneous costs.

Cut down on unnecessary expenses

Once you have created your budget plan, it’s time to cut down on unnecessary expenses. This includes dining out, buying clothes you don’t need, and subscription services you rarely use. Instead, focus on spending on essential items and prioritize your expenses accordingly.

Plan your meals in advance

Planning your meals can help you save significant money. For example, list the groceries you need for the week and avoid impulse purchases. Additionally, you can opt for budget-friendly meals and make use of leftovers.

Avoid unnecessary debt

Avoid taking on unnecessary debt and always pay your bills on time. This will help you avoid late fees and penalties, which can add up to a significant amount over time. In addition, if you have existing debt, pay it off as soon as possible to avoid accruing additional interest charges.

Reduce energy consumption

Reducing your energy consumption can help you save significant money on your utility bills. You can do this by turning off lights and appliances when not in use, using energy-efficient light bulbs, and reducing water usage.

Consider refinancing your mortgage

If you have a mortgage, consider refinancing it to a lower interest rate. This can help you save on monthly mortgage payments and free up extra cash for other expenses.

Find ways to earn extra income

Finding ways to earn extra income can also help you maintain a healthy budget at home. For example, you can take on a part-time or freelancing job, sell unwanted items online, or offer your skills and services to others.

Use coupons and discount codes

Using coupons and discount codes can help you save money on your purchases. Look for online deals and coupon codes before purchasing, and take advantage of sales and promotional offers.

Invest in home maintenance

Investing in home maintenance can help you avoid costly repairs and replacements in the future. Regularly cleaning and maintaining your home appliances and systems can also help you save money on your utility bills.

Set financial goals

Finally, setting financial goals can help you stay motivated and focused on maintaining a healthy budget at home. Whether saving for a vacation or paying off debt, having a clear plan can help you prioritize your expenses and make smart financial decisions.

In conclusion, maintaining a healthy budget at home requires discipline, planning, and intelligent financial decisions. By following these tips, you can reduce your expenses, avoid unnecessary debt, and save money for the future.

Being a single parent in tough economic times

As a sole caretaker, it can be a challenge to make both ends meet, particularly during challenging economic times. You might find yourself struggling to cover bills, put food on the table, and care for your children. However, rest assured that there are strategies to move forward even during these trying times. In this composition, we will provide you with some pointers and guidance on how to progress as a single parent during challenging economic periods.

- Devise a Financial Plan The first move to making progress as a single parent is to devise a financial plan. Although this may seem self-evident, numerous people do not take the time to design a budget, and they wind up overspending. A budget will assist you in tracking your income and expenditures, guaranteeing that you do not spend more than you can afford. It will also assist you in identifying areas where you can cut back on spending.

- Economize Once you have a budget in place, it is essential to economize wherever possible. This may include cutting down on unnecessary expenses, such as dining out or buying pricey clothing. It can also imply finding methods to save money on necessities, such as groceries and utilities. Look for coupons, buy in bulk, and switch to energy-efficient appliances to save money on your monthly bills.

- Boost Your Income One of the best ways to make progress as a single parent is to increase your income. This can be achieved in various ways, such as taking on a second job, freelancing, or starting a small business. It may also be worth considering returning to school to acquire new abilities that will make you more marketable in your field.

- Take Advantage of Government Assistance Programs Numerous government assistance programs are accessible to single parents that can assist you in making progress. These programs can provide financial assistance, childcare assistance, and even job training. Conduct research on the programs available in your locality and take advantage of them if you qualify.

- Develop a Support System Being a sole caretaker can be lonely and overwhelming at times. That is why it is crucial to develop a support system of friends and family who can assist you through the difficult times. Joining a single-parent support group can also be beneficial, as it will provide you with the chance to connect with other single parents who are undergoing similar experiences.

In conclusion, making progress as a single parent during difficult economic times necessitates meticulous planning, hard work, and a willingness to seek assistance when required. By devising a budget, economizing, boosting your income, taking advantage of government assistance programs, and developing a support system, you can overcome the challenges of being a sole caretaker and attain financial stability.

Money Troubles: A Parent’s Guide to Overcoming Debt from an Overspending Adult Child

As a responsible parent, it can be quite a stress-inducing predicament when your adult offspring’s expenditure begins to saddle you with debt. It’s a complex conundrum, but imperative that you take command of the situation and make the required alterations to enhance your financial well-being. This composition will furnish you with some practical suggestions and guidance on what you can do when your adult child’s spending causes you debt.

Understanding the issue

To solve any predicament, you must first comprehend it. You need to fathom why your adult child’s spending is resulting in debt for you. It could be that they’re splurging on unnecessary purchases, living beyond their means, or simply not contributing enough to the household expenses. Whatever the cause may be, it’s crucial to have a candid and transparent discussion with your child to comprehend their stance and work towards a resolution.

Establishing limits and expectations

Once you’ve had an honest conversation with your grown-up child, it’s crucial to establish unequivocal limits and expectations. Inform them of what you anticipate in terms of their financial contributions and how much you’re willing to aid them. It’s also vital to set limits on their spending and help them grasp the impact it has on your finances. By defining clear boundaries and expectations, you can sidestep any misunderstandings and ensure that everyone is on the same wavelength.

Assisting your child in managing their finances

If your adult child is struggling to manage their finances, you can offer your assistance. You can provide them with financial counsel, help them construct a budget, and educate them on effective money management. By aiding your child in managing their finances, you’ll not only be supporting them but also preventing any future financial stress on yourself.

Devising a debt repayment plan

If you’re already in debt due to your adult child’s spending habits, it’s imperative to formulate a repayment plan. You can begin by assessing your current financial status, creating a budget, and identifying areas where you can curtail expenses. It’s also crucial to prioritize your debts and focus on repaying the debts with the highest interest rates first. By formulating a debt repayment plan, you can take command of your finances and enhance your financial well-being.

In conclusion, dealing with your adult child’s spending habits can be a taxing situation, but it’s essential to take command of the situation and make the required changes to improve your financial well-being. By comprehending the issue, establishing limits and expectations, assisting your child in managing their finances, and devising a plan to pay off the debt, you can navigate this challenging predicament and emerge with your financial well-being intact.